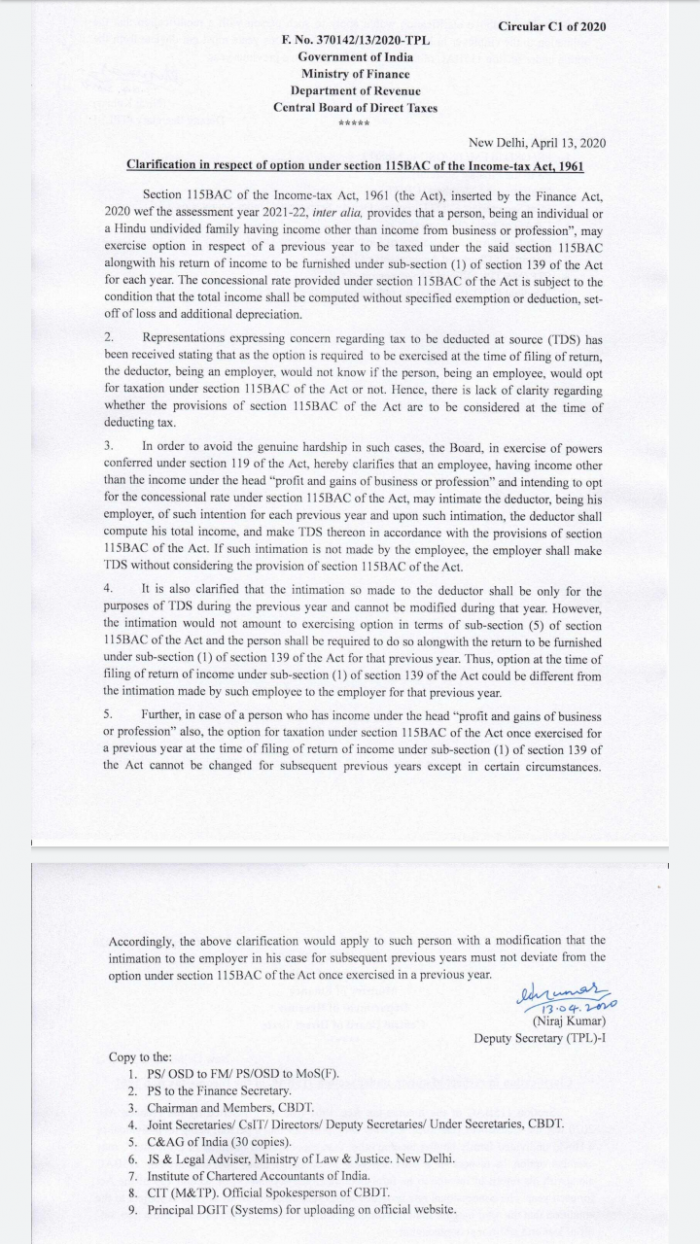

There’s so much fuss about the new Code on Wages implementation and how to restructure the compensation to be compliant. While the general guideline is to have at least 50% of the salary as Basic Pay, what if you do not keep it so?

Well, while it is recommended that you keep 50% of the total pay as Basic Pay, even if you do not keep it that way, it should not bother you much. In cases where Basic Pay is less than 50%, then the Basic Pay for calculation of other benefits (such as leave encashments, Gratuity, etc.) should be based on the 50% of the salary. This would mean, effectively, allowances cannot be more than 50%, technically or practically—even if you do not restructure the compensation.

However, with that preface, let’s look at some salary structures that one can probably include while making an offer to a prospective candidate (beware: if you are making changes to an existing employee’s compensation, there are things to be careful about) so that there are tax-efficient components:

- House Rent Allowance is IT-exempt subject to the Income Tax rules, upto 40% of the Basic Pay in non-metro cities and up to 50% of the Basic Pay (+DA) in Metro Cities. The exact amount of exemption is the minimum of the following three (though you are welcome to have an even higher amount being shown as HRA in the salary structure, it won’t have any impact on the tax exemption):

a) Actual HRA received from employer (that is shown on the payslip)

b) 40% or 50% of Basic Pay (+DA) depending on the nature of the city

c) Actual rent paid minus 10% of Basic Salary (+DA)

- Leave Travel Allowance is IT-exempt subject to the Income Tax rules, and subject to production of proofs as mandated by the Income Tax department. For the exemption to be effective, the payslip should have a component “LTA”. There is no specified limit on the % of LTA, but typically companies follow 5%-8.33% of Basic Pay (+DA) as the LTA amount. List of accepted expenses as LTA proof; note that LTA exemptions are not financial-year based, but based on a block of four calendar years (current block year: 2022-25).

- Books & Periodicals Reimbursements: Companies are welcome to include this as a reimbursement component of their total compensation and show it on payslips. They are welcome to provide reimbursement for the books and periodicals that are pertinent to the nature of jobs of the employees, against submission of relevant proofs. While there are no specified limits on this, companies usually tend to keep it in the range of Rs. 1000—2500 per month; senior professionals may be given a higher amount of reimbursement depending up on their role.

- Telephone & Internet Reimbursements: Similar on the lines of Books & Periodicals Reimbursements

- Fuel and Vehicle Maintenance Reimbursements: This is typically provided to senior leaders in companies, who may have to utilise their cars for business-related intents. Up to Rs. 2400/- per month against proper records of travels and fuel/maintenance receipts.

- Professional Development Allowance: Companies can reimburse the cost of courses/training/certification/professional memberships whose expenses are met from the pocket of the employee, against sufficient proofs. Such expenses could be mandated to be directly related to their role at the organistaion and have sane guidelines for which expenses can be considered.

- Annual Gift Voucher: Digital or physical gift coupons to the tune of Rs. 5000/- can be given to employees per a financial year, which is income tax-exempt. No proofs are usually required.

- Food Coupons: they can be paid in the form of physical or digital coupons/card and are exempt from Income Tax (usually not paid through payroll since cash as such is not being disbursed). No proofs are usually required. Maximum limit per month: Rs. 2500/- depending on the number of days your office operates.

- Children Education Allowance: Upto Rs. 100/- per month per child (for a maximum of 2 children per employee) is tax exempt under this category. This benefit can be provided for employees with children only. This does NOT limit employee’s 80C exemption of Children’s Tuition Fees.

- Hostel Expenditure Allowance: Up to Rs. 300/- per month per child (for a maximum of 2 children per employee) is tax-exempt under this category.

- Uniform Allowance: Applicable if there is a uniform at work.

- Include employee/employer contributions such as Corporate NPS

- Other means of executive compensation: Executive compensations are another realm, which may include more “benefits” than in the form of “pay components” and hence not delving into those areas now.

Word of caution: While designing the salary structure, the intent should NOT be tax avoidance or tax evasion, but utilising the existing legal provisions to form a tax-efficient structure. In the cases where it is mentioned above that proofs are required, you are still welcome to disburse that part of compensation if the employees do not have proof, but that will attract income tax.

A sample salary structure is provided below (not all of them could apply to you or to a specific employee), for illustration purposes only. Consult your legal team before you implement.

| Component | Amount per month | Amount per year |

| Basic Pay | ₹40,000 | ₹480,000 |

| HRA | ₹16,000 | ₹192,000 |

| LTA | ₹3,332 | ₹39,984 |

| Internet and Telephone Reim | ₹1,000 | ₹12,000 |

| Books and Periodicals Reim | ₹1,000 | ₹12,000 |

| Fuel and Vehicle Maintenance Reim | ₹2,400 | ₹28,800 |

| Professional Development Reim | ₹2,000 | ₹24,000 |

| Food Coupons | ₹2,500 | ₹30,000 |

| Annual Gift Coupon | ₹0 | ₹5,000 |

| Children Education Allowance | ₹100 | ₹1,200 |

| Hostel Expenditure Allowance | ₹300 | ₹3,600 |

| Special Allowance | ₹10,951 | ₹131,412 |

| Gross Salary | ₹959,996 | |

| Employer Contributions | ||

| Employer Contribution to EPF | ₹4,800 | ₹57,600 |

| Employer Contribution to LWF | ₹20.00 | ₹240.00 |

| Employer Contribution to NPS | ₹4,000.00 | ₹48,000.00 |

| Cost to Company (CTC) | ₹1,065,836 |

Here’s the excel sheet with the above salary structure, for download.

Disclaimer: The views in this article are provided personal and for academic purposes only. They need not reflect the views of my employer/previous employer(s).

Images sourced from: unsplash.com