[Download the checklist at the end of this article]

Are you looking for a payroll (managed) partner in India? It can be overwhelming as to what aspects to be mindful of in the process.

Here is a set of questions that you can consider to ask the vendors you have shortlisted. Not all of these questions may be applicable to all organisations and not all questions are on this document either.

Below are some abstract set of questions and a detailed set of questions are provided at the end of this article for you to download.

Input and Output

Starting with how the input-output communications occur, their cadence, mode of communication, how results are presented, availability of various reports, pay structuring and support for pay components, monthly or year-end TDS process, etc. can be points of discussion. How about new joiners and leavers?

Admin

Whether the partner allows admin access to the payroll platform to select employees of the client organisation, what kind of reports can be generated by the admin, etc. can be thought of before taking a decision.

ESS

Will employees get access to an Employee Self-Service portal where they can see their pay details, and tax calculations, declare investments, download payslips, submit reimbursements and year-end proofs, etc.? Well, this is important for employee experience and should be considered as a serious point of discussion. Questions like whether there is a mobile app for the ESS is also good question to ask.

Payslips

How customisable are the payslip structure and formats? Can the client organisation’s branding guidelines be followed? What information (such as PF#, UAN, LWF#, PAN, Bank Account#, etc.) can be shown on the payslip?

Integration

Can the payroll partner integrate their tool into the client organisation’s HRIS? How about various documents such as Payslips, Form 16, etc.? Will they appear on the HRIS as well? How about compensation analytics and tax projections?

Compliances

Can the payroll partner take care of EPF/ESI/PT/LWF payments, returns, etc.? How about the other labour law returns/forms to be kept/registrations to be taken? Or, will the client organisation have to engage another service provider for these services?

There’s so much fuss about the new Code on Wages implementation and how to restructure the compensation to be compliant. While the general guideline is to have at least 50% of the salary as Basic Pay, what if you do not keep it so?

Well, while it is recommended that you keep 50% of the total pay as Basic Pay, even if you do not keep it that way, it should not bother you much. In cases where Basic Pay is less than 50%, then the Basic Pay for calculation of other benefits (such as leave encashments, Gratuity, etc.) should be based on the 50% of the salary. This would mean, effectively, allowances cannot be more than 50%, technically or practically—even if you do not restructure the compensation.

However, with that preface, let’s look at some salary structures that one can probably include while making an offer to a prospective candidate (beware: if you are making changes to an existing employee’s compensation, there are things to be careful about) so that there are tax-efficient components:

Tax-avoidance or tax-escaping is not the way; but tax-efficiency is the one.

House Rent Allowance is IT-exempt subject to the Income Tax rules, upto 40% of the Basic Pay in non-metro cities and up to 50% of the Basic Pay (+DA) in Metro Cities. The exact amount of exemption is the minimum of the following three (though you are welcome to have an even higher amount being shown as HRA in the salary structure, it won’t have any impact on the tax exemption):

a) Actual HRA received from employer (that is shown on the payslip) b) 40% or 50% of Basic Pay (+DA) depending on the nature of the city c) Actual rent paid minus 10% of Basic Salary (+DA)

Leave Travel Allowance is IT-exempt subject to the Income Tax rules, and subject to production of proofs as mandated by the Income Tax department. For the exemption to be effective, the payslip should have a component “LTA”. There is no specified limit on the % of LTA, but typically companies follow 5%-8.33% of Basic Pay (+DA) as the LTA amount. List of accepted expenses as LTA proof; note that LTA exemptions are not financial-year based, but based on a block of four calendar years (current block year: 2022-25).

Books & Periodicals Reimbursements: Companies are welcome to include this as a reimbursement component of their total compensation and show it on payslips. They are welcome to provide reimbursement for the books and periodicals that are pertinent to the nature of jobs of the employees, against submission of relevant proofs. While there are no specified limits on this, companies usually tend to keep it in the range of Rs. 1000—2500 per month; senior professionals may be given a higher amount of reimbursement depending up on their role.

Telephone & Internet Reimbursements: Similar on the lines of Books & Periodicals Reimbursements

Fuel and Vehicle MaintenanceReimbursements: This is typically provided to senior leaders in companies, who may have to utilise their cars for business-related intents. Up to Rs. 2400/- per month against proper records of travels and fuel/maintenance receipts.

Professional Development Allowance: Companies can reimburse the cost of courses/training/certification/professional memberships whose expenses are met from the pocket of the employee, against sufficient proofs. Such expenses could be mandated to be directly related to their role at the organistaion and have sane guidelines for which expenses can be considered.

Annual Gift Voucher: Digital or physical gift coupons to the tune of Rs. 5000/- can be given to employees per a financial year, which is income tax-exempt. No proofs are usually required.

Food Coupons: they can be paid in the form of physical or digital coupons/card and are exempt from Income Tax (usually not paid through payroll since cash as such is not being disbursed). No proofs are usually required. Maximum limit per month: Rs. 2500/- depending on the number of days your office operates.

Children Education Allowance: Upto Rs. 100/- per month per child (for a maximum of 2 children per employee) is tax exempt under this category. This benefit can be provided for employees with children only. This does NOT limit employee’s 80C exemption of Children’s Tuition Fees.

Hostel Expenditure Allowance: Up to Rs. 300/- per month per child (for a maximum of 2 children per employee) is tax-exempt under this category.

Uniform Allowance: Applicable if there is a uniform at work.

Include employee/employer contributions such as Corporate NPS

Other means of executive compensation: Executive compensations are another realm, which may include more “benefits” than in the form of “pay components” and hence not delving into those areas now.

Slicing the total compensation at the right measures is the key to a tax-efficient salary structure

Word of caution: While designing the salary structure, the intent should NOT be tax avoidance or tax evasion, but utilising the existing legal provisions to form a tax-efficient structure. In the cases where it is mentioned above that proofs are required, you are still welcome to disburse that part of compensation if the employees do not have proof, but that will attract income tax.

A sample salary structure is provided below (not all of them could apply to you or to a specific employee), for illustration purposes only. Consult your legal team before you implement.

Component

Amount per month

Amount per year

Basic Pay

₹40,000

₹480,000

HRA

₹16,000

₹192,000

LTA

₹3,332

₹39,984

Internet and Telephone Reim

₹1,000

₹12,000

Books and Periodicals Reim

₹1,000

₹12,000

Fuel and Vehicle Maintenance Reim

₹2,400

₹28,800

Professional Development Reim

₹2,000

₹24,000

Food Coupons

₹2,500

₹30,000

Annual Gift Coupon

₹0

₹5,000

Children Education Allowance

₹100

₹1,200

Hostel Expenditure Allowance

₹300

₹3,600

Special Allowance

₹10,951

₹131,412

Gross Salary

₹959,996

Employer Contributions

Employer Contribution to EPF

₹4,800

₹57,600

Employer Contribution to LWF

₹20.00

₹240.00

Employer Contribution to NPS

₹4,000.00

₹48,000.00

Cost to Company (CTC)

₹1,065,836

Tax-efficient Salary Structuring: An Example

Here’s the excel sheet with the above salary structure, for download.

Disclaimer: The views in this article are provided personal and for academic purposes only. They need not reflect the views of my employer/previous employer(s).

Much has been said and written about National Pension System (NPS) already. The intention of this article is to give a quick idea to my fellow HRs in the network as to why this is a great benefit you can offer to your employees. Non-HR folks reading this—check with your HR team to see if this is an option at your organisation if you don’t already have it.

What is NPS?

As the name suggests, it is National Pension System. The Govt. of India introduced it for the central and government employees but a few years ago it was extended for the Private Sector employees (and for any citizen of age 15-65, for that matter irrespective of whether they are employed) as well. It is a voluntary pension fund (+wealth creation fund, I might add). Employees can contribute amounts to the NPS fund which will be invested in equity stocks, government bonds, corporate debts, etc.

When does the pension start?

At the time of maturity, one can withdraw up to 60% of the lumpsum. The balance 40% should be invested in annuity (pension), which will be used to give you pension for the rest of your life. One has an option to put in any percentage above 60% up to 100% to the annuity, too. Here’s an NPS calculator.

Can you tell me a little bit more about NPS?

I will skip that part since numerous websites have already written about it—NPS Trust’s website or Wikipedia can be a starter. There are many youtube videos on the topic too. You should be able to read/watch pros and cons of the scheme.

Each bit that you save now will keep your golden years safer

How are the returns?

Better than EPF in terms of absolute profit from invested corpus, from the stats. Dig in here and here’s Scheme E’s returns. The minimum contribution in a financial year to keep the account active is Rs. 1000/-.

How can I join NPS?

Simple. Join here online. Keep digital copies of your PAN, Photograph, Aadhaar and cancelled cheque/bank account passbook with you. The cancelled cheque/bank account passbook should bear your name.

Is contribution to NPS tax-exempt?

Yes, it is exempt in your 80C (and 80CCC, 80CCD(1)). Plus, there is a special exemption of Rs. 50,000/- for NPS contributions under 80CCD(1B). Contributions to NPS is Exempt-Exempt-Exempt, i.e. tax-exempt at the tie of contribution, tax-exempt on the profit earned on an investment, and tax-exempt at the time of maturity (conditions apply).

Well, is it fully tax-exempt?

Your investment is fully tax-exempt at the time of investment. Your return every year that is being added back to NPS corpus is tax-exempt. Your corpus is, well, hmm… two things: exempt for the part that goes to annuity and the rest (that you withdraw) is not exempt. One cannot say that NPS is fully non-taxable at the time of maturity in that sense.

Now tell me, how’s NPS and Corporate NPS different?

Corporate NPS is NPS whose contributions are made through the employer. Instead of you making direct contribution to your NPS fund, you ask your employer to deduct a certain amount from your CTC and contribute to your NPS.

What’s the advantage of having Corporate NPS?

Contributions made through Corporates are tax-exempt under 80CCD(2) for up to 10% of Basic Pay of the employee. That is, if your annual basic pay is Rs. 10 Lakhs, then a contribution up to Rs. 1 Lakh per year is fully tax-free. This is over and above your 80C, 80CCC, 80CCD(1) and 80CCD(1B). Meaning, you still can invest into NPS on your own as per the above sections and claim those tax-exemptions as well, besides the corporate contributions made.

That’s exciting. How can corporates register for Corporate NPS?

Corporates will have to find a PFM and POP. Ask your HR or Finance team to reach out to them and the rest of the onboarding will be taken care of by them. It will need very minimal involvement by your HR/Finance team. Make sure that you choose the PFMs after due diligence (look at peer feedbacks, return rates, etc.).

NPS is one way of saving money for your retirement.

How can we connect employees NPS ID to our corporate NPS?

You should ask employees to provide their NPS (the same NPS ID—known as PRAN—created for their direct investment shall be used for Corporate NPS contributions as well). Provide these PRANs to your PFM and they will link it to your corporate account.

How does this play with salary structuring?

Corporate NPS contributions usually form part of the employer contributions of the CTC. If your offer/appointment letter allows flexibility of revising the salary structure (perhaps at the request of the employee), this is a great benefit to add. You may even offer a choice for the employee to choose an amount up to 10% of their monthly basic pay to be contributed every month (going above 10% won’t be beneficial in terms of tax-exemption). You may also consider providing this as an additional benefit to the existing employer contributions, if the company financials are good, thereby not touching the gross pay.

If Corporate NPS cannot be offered to your current employees owing to a rigid offer/appointment letter, consider offering this as a choosable perk to future employees. They will love it when they see the returns plus the taxes being saved.

Hey, I see options like Aggressive (LC75), LC50 and such. What are they?

These options indicate how aggressive the investments are. LC75, for example, says 75% of the contributions will be invested in equity, while the balance will be in government bonds/corporate debt funds. LC50 would mean and 50% contribution to equity funds. Though corporates can set the nature of aggressiveness at the start of the Corporate NPS, employees will have an option to set their own aggressiveness (and can even change the PFMs for their own fund) after a stipulated time (~1 year).

If your workforce is generally young, say less than 35 years of age, LC75 would not hurt much. If your workforce is comparatively older, say above 40, it’s safe to stay with less-riskier options such as LC50.

What are the cons of NPS?

There could be multiple legs: NPS is a market-linked product and hence the market fluctuations can affect your returns. You will still need to manage your PMS once in a while to make sure that you have higher/steady returns — this needs manual intervention from the investor. Plus, the government still require the investor to keep at least 40% of the maturity corpus to be invested in annuity, whose returns are not at par with the inflation. More here.

This article is also published on LinkedIn and Medium.

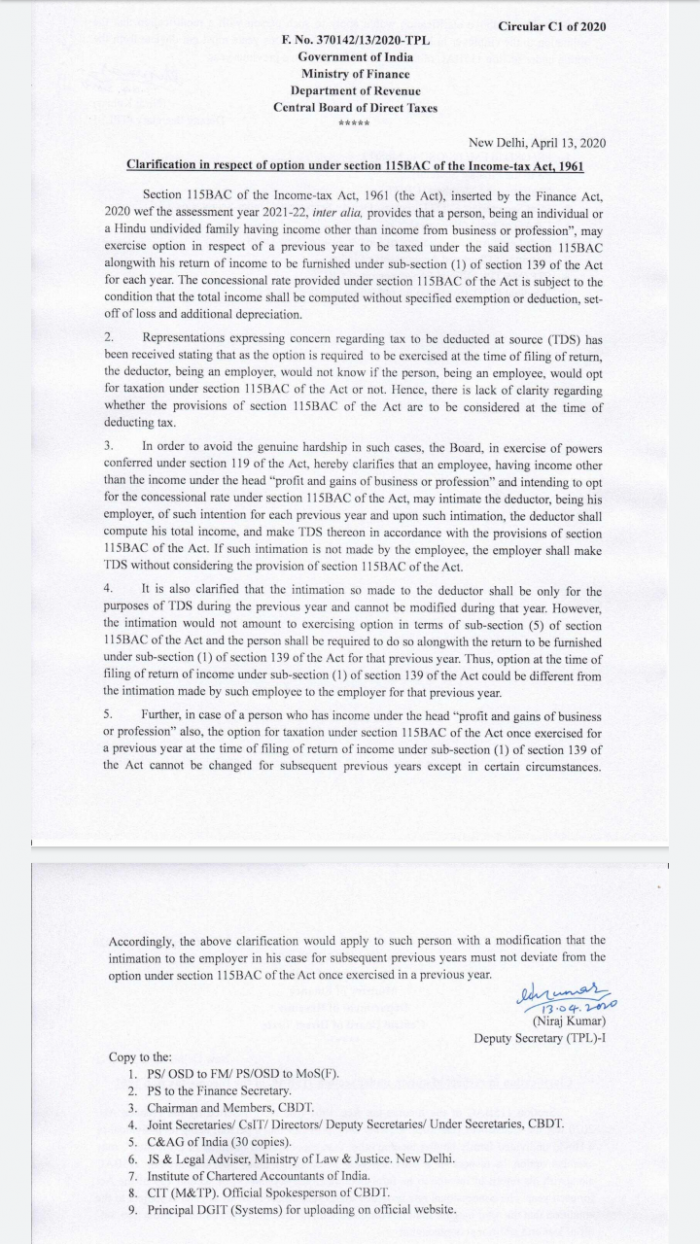

Update (Apr 13, 2020): Govt of India has clarified that the employee can ask deductor (employer) to consider new tax regime for taxation (provided certain conditions of no-business income, etc. are met). The notification below is just in. Thanks to Ankit Lohiya for updating me about the notification.

Hence, the article below stands void.

In the 2020-21 budget by the Govt of India, a new tax regime was announced. The below table depicts the difference between the old regime and the new regime. HOWEVER, Govt has announced that it will give an option for the citizens to choose which tax regime they would like to be taxed on.

Does that mean I can tell my employer to tax me on which regime?

As it looks, your employer cannot take such an option from you to choose which income tax regime they should tax you on.

So, what will the employer do?

The employer will still need to, as of today, continue deducting income taxes per the old regime (like how they used to do during FY 2019-20). They cannot ask, or take a choice from, the employee on which regime to tax on, nor they can tax them other than on the old tax regime.

When can I then choose my tax regime?

The employee can choose the tax regime at the time of his/her Income Tax returns. The IT department will recalculate the income tax and ask you to pay/refund an additional amount.

Why is it that so? Why can’t employers take option from employees?

As per the Finance Act, 2020 which is enacted by the Parliament, taxes are to be withheld and paid to the Government as per Part I of First Schedule of the Act (please see screenshots below).

The Government has, in fact, introduced the new tax regime not by altering the Part I of First Schedule above, but instead by introducing the new regime as a new section (Section 115BAC). As long as Part I of First Schedule is changed/amended with the rates mentioned in 115BAC, the employer needs to follow the old regime for TDS.

Can I change choose old regime in the years to come, if I choose the new regime during FY 2020-21 (AY 2021-22) during income tax returns?

No, 115BAC mandates that in case of individuals and HUFs who have income either from a business or a profession, once this option is exercised, they will have to continue with the new regime for that year and all subsequent years.

(with inputs from multiple resources and people, including Sreelal).