[Download the checklist at the end of this article]

Are you looking for a payroll (managed) partner in India? It can be overwhelming as to what aspects to be mindful of in the process.

Here is a set of questions that you can consider to ask the vendors you have shortlisted. Not all of these questions may be applicable to all organisations and not all questions are on this document either.

Below are some abstract set of questions and a detailed set of questions are provided at the end of this article for you to download.

Input and Output

Starting with how the input-output communications occur, their cadence, mode of communication, how results are presented, availability of various reports, pay structuring and support for pay components, monthly or year-end TDS process, etc. can be points of discussion. How about new joiners and leavers?

Admin

Whether the partner allows admin access to the payroll platform to select employees of the client organisation, what kind of reports can be generated by the admin, etc. can be thought of before taking a decision.

ESS

Will employees get access to an Employee Self-Service portal where they can see their pay details, and tax calculations, declare investments, download payslips, submit reimbursements and year-end proofs, etc.? Well, this is important for employee experience and should be considered as a serious point of discussion. Questions like whether there is a mobile app for the ESS is also good question to ask.

Payslips

How customisable are the payslip structure and formats? Can the client organisation’s branding guidelines be followed? What information (such as PF#, UAN, LWF#, PAN, Bank Account#, etc.) can be shown on the payslip?

Integration

Can the payroll partner integrate their tool into the client organisation’s HRIS? How about various documents such as Payslips, Form 16, etc.? Will they appear on the HRIS as well? How about compensation analytics and tax projections?

Compliances

Can the payroll partner take care of EPF/ESI/PT/LWF payments, returns, etc.? How about the other labour law returns/forms to be kept/registrations to be taken? Or, will the client organisation have to engage another service provider for these services?

There’s so much fuss about the new Code on Wages implementation and how to restructure the compensation to be compliant. While the general guideline is to have at least 50% of the salary as Basic Pay, what if you do not keep it so?

Well, while it is recommended that you keep 50% of the total pay as Basic Pay, even if you do not keep it that way, it should not bother you much. In cases where Basic Pay is less than 50%, then the Basic Pay for calculation of other benefits (such as leave encashments, Gratuity, etc.) should be based on the 50% of the salary. This would mean, effectively, allowances cannot be more than 50%, technically or practically—even if you do not restructure the compensation.

However, with that preface, let’s look at some salary structures that one can probably include while making an offer to a prospective candidate (beware: if you are making changes to an existing employee’s compensation, there are things to be careful about) so that there are tax-efficient components:

Tax-avoidance or tax-escaping is not the way; but tax-efficiency is the one.

House Rent Allowance is IT-exempt subject to the Income Tax rules, upto 40% of the Basic Pay in non-metro cities and up to 50% of the Basic Pay (+DA) in Metro Cities. The exact amount of exemption is the minimum of the following three (though you are welcome to have an even higher amount being shown as HRA in the salary structure, it won’t have any impact on the tax exemption):

a) Actual HRA received from employer (that is shown on the payslip) b) 40% or 50% of Basic Pay (+DA) depending on the nature of the city c) Actual rent paid minus 10% of Basic Salary (+DA)

Leave Travel Allowance is IT-exempt subject to the Income Tax rules, and subject to production of proofs as mandated by the Income Tax department. For the exemption to be effective, the payslip should have a component “LTA”. There is no specified limit on the % of LTA, but typically companies follow 5%-8.33% of Basic Pay (+DA) as the LTA amount. List of accepted expenses as LTA proof; note that LTA exemptions are not financial-year based, but based on a block of four calendar years (current block year: 2022-25).

Books & Periodicals Reimbursements: Companies are welcome to include this as a reimbursement component of their total compensation and show it on payslips. They are welcome to provide reimbursement for the books and periodicals that are pertinent to the nature of jobs of the employees, against submission of relevant proofs. While there are no specified limits on this, companies usually tend to keep it in the range of Rs. 1000—2500 per month; senior professionals may be given a higher amount of reimbursement depending up on their role.

Telephone & Internet Reimbursements: Similar on the lines of Books & Periodicals Reimbursements

Fuel and Vehicle MaintenanceReimbursements: This is typically provided to senior leaders in companies, who may have to utilise their cars for business-related intents. Up to Rs. 2400/- per month against proper records of travels and fuel/maintenance receipts.

Professional Development Allowance: Companies can reimburse the cost of courses/training/certification/professional memberships whose expenses are met from the pocket of the employee, against sufficient proofs. Such expenses could be mandated to be directly related to their role at the organistaion and have sane guidelines for which expenses can be considered.

Annual Gift Voucher: Digital or physical gift coupons to the tune of Rs. 5000/- can be given to employees per a financial year, which is income tax-exempt. No proofs are usually required.

Food Coupons: they can be paid in the form of physical or digital coupons/card and are exempt from Income Tax (usually not paid through payroll since cash as such is not being disbursed). No proofs are usually required. Maximum limit per month: Rs. 2500/- depending on the number of days your office operates.

Children Education Allowance: Upto Rs. 100/- per month per child (for a maximum of 2 children per employee) is tax exempt under this category. This benefit can be provided for employees with children only. This does NOT limit employee’s 80C exemption of Children’s Tuition Fees.

Hostel Expenditure Allowance: Up to Rs. 300/- per month per child (for a maximum of 2 children per employee) is tax-exempt under this category.

Uniform Allowance: Applicable if there is a uniform at work.

Include employee/employer contributions such as Corporate NPS

Other means of executive compensation: Executive compensations are another realm, which may include more “benefits” than in the form of “pay components” and hence not delving into those areas now.

Slicing the total compensation at the right measures is the key to a tax-efficient salary structure

Word of caution: While designing the salary structure, the intent should NOT be tax avoidance or tax evasion, but utilising the existing legal provisions to form a tax-efficient structure. In the cases where it is mentioned above that proofs are required, you are still welcome to disburse that part of compensation if the employees do not have proof, but that will attract income tax.

A sample salary structure is provided below (not all of them could apply to you or to a specific employee), for illustration purposes only. Consult your legal team before you implement.

Component

Amount per month

Amount per year

Basic Pay

₹40,000

₹480,000

HRA

₹16,000

₹192,000

LTA

₹3,332

₹39,984

Internet and Telephone Reim

₹1,000

₹12,000

Books and Periodicals Reim

₹1,000

₹12,000

Fuel and Vehicle Maintenance Reim

₹2,400

₹28,800

Professional Development Reim

₹2,000

₹24,000

Food Coupons

₹2,500

₹30,000

Annual Gift Coupon

₹0

₹5,000

Children Education Allowance

₹100

₹1,200

Hostel Expenditure Allowance

₹300

₹3,600

Special Allowance

₹10,951

₹131,412

Gross Salary

₹959,996

Employer Contributions

Employer Contribution to EPF

₹4,800

₹57,600

Employer Contribution to LWF

₹20.00

₹240.00

Employer Contribution to NPS

₹4,000.00

₹48,000.00

Cost to Company (CTC)

₹1,065,836

Tax-efficient Salary Structuring: An Example

Here’s the excel sheet with the above salary structure, for download.

Disclaimer: The views in this article are provided personal and for academic purposes only. They need not reflect the views of my employer/previous employer(s).

Much has been said and written about National Pension System (NPS) already. The intention of this article is to give a quick idea to my fellow HRs in the network as to why this is a great benefit you can offer to your employees. Non-HR folks reading this—check with your HR team to see if this is an option at your organisation if you don’t already have it.

What is NPS?

As the name suggests, it is National Pension System. The Govt. of India introduced it for the central and government employees but a few years ago it was extended for the Private Sector employees (and for any citizen of age 15-65, for that matter irrespective of whether they are employed) as well. It is a voluntary pension fund (+wealth creation fund, I might add). Employees can contribute amounts to the NPS fund which will be invested in equity stocks, government bonds, corporate debts, etc.

When does the pension start?

At the time of maturity, one can withdraw up to 60% of the lumpsum. The balance 40% should be invested in annuity (pension), which will be used to give you pension for the rest of your life. One has an option to put in any percentage above 60% up to 100% to the annuity, too. Here’s an NPS calculator.

Can you tell me a little bit more about NPS?

I will skip that part since numerous websites have already written about it—NPS Trust’s website or Wikipedia can be a starter. There are many youtube videos on the topic too. You should be able to read/watch pros and cons of the scheme.

Each bit that you save now will keep your golden years safer

How are the returns?

Better than EPF in terms of absolute profit from invested corpus, from the stats. Dig in here and here’s Scheme E’s returns. The minimum contribution in a financial year to keep the account active is Rs. 1000/-.

How can I join NPS?

Simple. Join here online. Keep digital copies of your PAN, Photograph, Aadhaar and cancelled cheque/bank account passbook with you. The cancelled cheque/bank account passbook should bear your name.

Is contribution to NPS tax-exempt?

Yes, it is exempt in your 80C (and 80CCC, 80CCD(1)). Plus, there is a special exemption of Rs. 50,000/- for NPS contributions under 80CCD(1B). Contributions to NPS is Exempt-Exempt-Exempt, i.e. tax-exempt at the tie of contribution, tax-exempt on the profit earned on an investment, and tax-exempt at the time of maturity (conditions apply).

Well, is it fully tax-exempt?

Your investment is fully tax-exempt at the time of investment. Your return every year that is being added back to NPS corpus is tax-exempt. Your corpus is, well, hmm… two things: exempt for the part that goes to annuity and the rest (that you withdraw) is not exempt. One cannot say that NPS is fully non-taxable at the time of maturity in that sense.

Now tell me, how’s NPS and Corporate NPS different?

Corporate NPS is NPS whose contributions are made through the employer. Instead of you making direct contribution to your NPS fund, you ask your employer to deduct a certain amount from your CTC and contribute to your NPS.

What’s the advantage of having Corporate NPS?

Contributions made through Corporates are tax-exempt under 80CCD(2) for up to 10% of Basic Pay of the employee. That is, if your annual basic pay is Rs. 10 Lakhs, then a contribution up to Rs. 1 Lakh per year is fully tax-free. This is over and above your 80C, 80CCC, 80CCD(1) and 80CCD(1B). Meaning, you still can invest into NPS on your own as per the above sections and claim those tax-exemptions as well, besides the corporate contributions made.

That’s exciting. How can corporates register for Corporate NPS?

Corporates will have to find a PFM and POP. Ask your HR or Finance team to reach out to them and the rest of the onboarding will be taken care of by them. It will need very minimal involvement by your HR/Finance team. Make sure that you choose the PFMs after due diligence (look at peer feedbacks, return rates, etc.).

NPS is one way of saving money for your retirement.

How can we connect employees NPS ID to our corporate NPS?

You should ask employees to provide their NPS (the same NPS ID—known as PRAN—created for their direct investment shall be used for Corporate NPS contributions as well). Provide these PRANs to your PFM and they will link it to your corporate account.

How does this play with salary structuring?

Corporate NPS contributions usually form part of the employer contributions of the CTC. If your offer/appointment letter allows flexibility of revising the salary structure (perhaps at the request of the employee), this is a great benefit to add. You may even offer a choice for the employee to choose an amount up to 10% of their monthly basic pay to be contributed every month (going above 10% won’t be beneficial in terms of tax-exemption). You may also consider providing this as an additional benefit to the existing employer contributions, if the company financials are good, thereby not touching the gross pay.

If Corporate NPS cannot be offered to your current employees owing to a rigid offer/appointment letter, consider offering this as a choosable perk to future employees. They will love it when they see the returns plus the taxes being saved.

Hey, I see options like Aggressive (LC75), LC50 and such. What are they?

These options indicate how aggressive the investments are. LC75, for example, says 75% of the contributions will be invested in equity, while the balance will be in government bonds/corporate debt funds. LC50 would mean and 50% contribution to equity funds. Though corporates can set the nature of aggressiveness at the start of the Corporate NPS, employees will have an option to set their own aggressiveness (and can even change the PFMs for their own fund) after a stipulated time (~1 year).

If your workforce is generally young, say less than 35 years of age, LC75 would not hurt much. If your workforce is comparatively older, say above 40, it’s safe to stay with less-riskier options such as LC50.

What are the cons of NPS?

There could be multiple legs: NPS is a market-linked product and hence the market fluctuations can affect your returns. You will still need to manage your PMS once in a while to make sure that you have higher/steady returns — this needs manual intervention from the investor. Plus, the government still require the investor to keep at least 40% of the maturity corpus to be invested in annuity, whose returns are not at par with the inflation. More here.

This article is also published on LinkedIn and Medium.

April 2021 is around the corner and there are a lot of buzz about the four new labour laws which are going to be in effect from Apr 1, 2021. One of them is Code on Wages and that’s effectively a revised version of Payment of Wages Act 1936, Minimum Wages Act 1948, Payment of Bonus Act 1965 and Equal Remuneration Act, 1976.

One of the major questions that HRs are facing these days is how the definitions are changing and how it’s going to affect the salary structures. It is their Y2K problem. Employees—who are not in the HR community—are worried as to how this is going to impact their take home salary, as depicted by some of the news outlets in the country.

Before we begin

Please make sure that you read my previous article on how salary structuring works (keep in mind that it was pre-Apr 2021). That article will help you understand various jargons in the Comp and Ben sector and make sure that you get the difference, inter alia, between Gross Pay, CTC, Employer Contributions, Employee Deductions, etc. Let’s call that article a prerequisite for this one.

Introduction

Code on Wages, along with the other three new labour laws, comes into effect from Apr 1, 2021; however, rules for all the four are not yet finalised and notified, but we hope that would happen soon so that they are in effect from the aforementioned date.

This article discusses some major impact these acts bring in to the Compensation and Benefits regime. I will focus more on the payroll structuring per se, rather than other major changes therein. Let’s dive in:

Structuring your salaries in the right way is crucial to make sure that both employees and employers benefit.

Definition of Wages

Definition of wages seemed to be one of the complicated definitions in the labour realm in India for many years. EPF Act defined wages differently than the ESI Act, and every other act in the country had its own definitions of Wages. With the new set of four consolidated labour laws in place, this confusion is removed. All the laws now provide a single definition of wages, as given below:

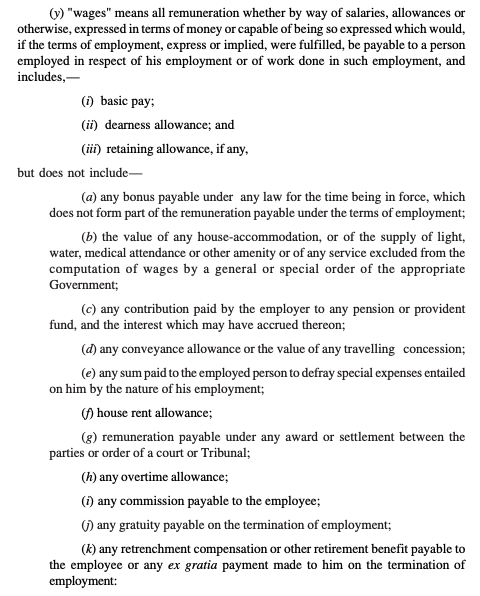

“wages” means all remuneration whether by way of salaries, allowances or otherwise, expressed in terms of money or capable of being so expressed which would, if the terms of employment, express or implied, were fulfilled, be payable to a person employed in respect of his employment or of work done in such employment, and includes,—

basic pay

dearness allowance and

retaining allowance

Further, the Code excludes the following components from the definition of wages: bonus payments;

any bonus payable under any law for the time being in force, which does not form part of the remuneration payable under the terms of employment;

the value of any house-accommodation, or of the supply of light, water, medical attendance or other amenity or of any service excluded from the computation of wages by a general or special order of the appropriate Government;

any contribution paid by the employer to any pension or provident fund, and the interest which may have accrued thereon;

any conveyance allowance or the value of any travelling concession;

any sum paid to the employed person to defray special expenses entailed on him by the nature of his employment;

house rent allowance;

remuneration payable under any award or settlement between the parties or order of a court or Tribunal;

any overtime allowance;

any commission payable to the employee;

any gratuity payable on the termination of employment;

any retrenchment compensation or other retirement benefit payable to the employee or any ex gratia payment made to him on the termination of employment

Excerpts from Code on Wages, 2019

Additional Clauses on Calculation of Wages

The goes on to state the following, which forms the crucial part while structuring salaries:

Provided that, for calculating the wages under this clause, if payments made by the employer to the employee under clauses (A) to (I) exceeds one-half, or such other per cent as may be notified by the Central Government, of the all remuneration calculated under this clause, the amount which exceeds such one-half, or the per cent so notified, shall be deemed as remuneration and shall be accordingly added in wages under this clause.

Provided further that for the purpose of equal wages to all genders and for the purpose of payment of wages, the emoluments specified in clauses (d), (f), (g) and (h) shall be taken for computation of wage.

Explanation.––Where an employee is given in lieu of the whole or part of the wages payable to him, any remuneration in kind by his employer, the value of such remuneration in kind which does not exceed fifteen per cent. of the total wages payable to him, shall be deemed to form part of the wages of such employee.

Reading the Clauses in the Act in Detail

It is evident that the Basic Pay is part of Wages.

DA, if it is part of the pay structure, it is included in Wages.

Retaining Allowance is also part of the Wages. It is to note that Retaining Allowance ≠ Special Allowance. You need to specifically provide this component and with the specific purposes thereof to make it Retaining Allowance, in the Offer Letter/Appointment Letters.

Gratuity, Statutory Bonus, HRA, ER EPF, ER ESI, OT, Commissions, and retrenchment compensation are excluded in the calculation of Wages.

Payment in kind such as payment for house accommodation (some companies provide free house accommodation for their employees for the initial few days or for a longer term) shall be excluded from Wages

Payment for special purposes shall be excluded from Wages

Dispute Settlements are excluded from Wages

Conveyance allowance is excluded from Wages.

The exclusion components should not be more than 50% (of the gross pay). If it is more than 50%, then the 50% of the gross pay shall be deemed to be the Wages.

HR and Finance need to work together to tackle this ‘Y2K problem for HRs’

Can the Inclusion Components (Wages) be more than 50%?

Yes. The act only says that the exclusion components should not be more than 50%. That clearly means that the inclusion components should be at least 50%. This also means that the Wages should be at least 50% of the gross pay. It can very well be above the 50% limit; and it can also be 100% of the salary. Provide the entire Gross Pay as Basic Pay, and no one will question you (though this is not ideal for both the employee and the employer).

Should Basic Pay be 50% of Gross Pay (or 50% of CTC)?

There are some articles that say the Basic Pay should be 50% of the CTC, which is wrong. The act only says that the exclusion components should not be more than 50% (= inclusion components should be at least 50%). That does NOT mean that the Basic pay should be 50% of Gross Pay.

Further, no acts in India talks about the CTC. It’s a term that our companies and accounting officers coined. When an act refers to the word salary, it, generally, means the gross pay.

Are all allowances excluded from Wages?

Just because a component has the word ‘allowance’ it is not excluded as such. You may want to revise how the definition of Wages begins: “wages” means all remuneration whether by way of salaries, allowances or otherwise. It essentially says that the word ‘allowance’ simply does not exclude it from Wages.

Is Special Allowance Excluded from Wages?

This is a hot and debated topic over the last few months. Indian companies use Special Allowance as a bucket to fill in to reach the CTC. That is, when the CTC is split into different components such as Basic Pay, HRA, etc. the remaining amount goes to Special Allowance so that they all add up to CTC. As long as your offer letter and/or the appointment letter does not have any specific definition (vide Exclusion List# E) related to Special Allowance, it is INCLUDED in the Wages. Here’s a presentation from Deloitte if you would like to have a look.

If you disagree with the above reading, please let me know in the comments and why.

Is HRA excluded from Wages?

Yes, HRA is excluded from the Wages Calculation.

Is Variable Pay included in Wages?

Performance-based variable pay will be an inclusion component in Wages, since that does not appear on the exclusion list.

So, what’s the big deal now?

The big deal is to make sure that your salary components are in line with the Code and that the Wages components is at least 50% of the Gross Pay. If your components are already in line with this math, you do not have to worry about restructuring at all. Peace!

Wait, can you tell me what all components can be there in a Salary Structure?

It would be unwise for an outsider to comment on how your components should be. However, below are some ordinarily paid salary structure components that one may find in the IT industry. I am trying to give you a comparison of those components with respect to the act.

Component

Included in Wages?

Taxable

Basic Pay

Yes

Yes

Dearness Allowance

Yes

Yes

HRA

No

Yes/No, subject to limits

Special Allowance

Yes

Yes

Conveyance Allowance

Yes

Yes

Telephone & Internet Expenses

No

Yes/No, subject to limits

Books & Periodical Expenses

No

Yes/No, subject to limits

Fuel and Vehicle Maintenance

No

Yes/No, subject to limits

Annual Gift Coupons

No

Yes/No, subject to limits

Monthly Food Coupons

No

Yes/No, subject to limits

Medical Allowance

No

Yes

Uniform Allowance

No

Yes/No, subject to limits

School Fee Allowance

No

Yes/No, subject to limits

My recommendation would be to choose the excluded components that may be relevant to job families and job roles in your organisation. If you have certain such components to defray special expenses already in your organisation, you won’t have to remove them and may not have to make much changes. The catch is that these components will help reduce your Wages (yet keeping at the minimum requirements) and help employees save some income tax (flexi benefits—more on that later).

One needs to design the inclusion and exclusion components in the salary structure in such a way that it is both compliant and comfortable.

Hey, what if the Wage goes high? Is there a Problem?

Well, as I mentioned before, the definition of Wages is now standardised. All the acts say that the benchmark on which retiral benefits and other such employee benefits are calculated will be based on Wages. Hence, from a financial point of view, it would be a good idea to look at where you need to keep the balance.

Some companies still continue to pay EPF on the Basic Pay (which may still be over and above the statutory limit of 1800). Such calculations of EPF, ESI, etc. will now be on the Wages component. Some companies may take a hit unless they restructure the salaries since a hike in Wages may imply a hike in employer contributions as well. Likewise, the Gratuity is currently based on Basic Pay, which may change from Apr 1, 2021, subject to final terms in the rules yet to be finalised. Similar is the case with Statutory Bonus as well, whose details are still not finalised. You may read the act for more information on these provisions; I am skipping the details since it may derail the purpose of this act.

Can you give me a sample salary structure?

Yes, I will. Let’s consider the IT industry in Kerala for example.

Component

Included in Wages?

Calculation

Amount (INR, Monthly)

Basic Pay (BP)

Yes

41.67% of Gross Pay

15,000

HRA

No

40% of B. Pay

6,000

Conveyance Allowance

No

2,000

Books & Periodical

No

2,500

Fuel & Vehicle Maintenance

No

2,400

Internet & Telephone

No

2,500

Monthly Food Coupons

No

2,500

Special Allowance (SA)

Yes

3,100

Gross Pay

36,000

Employer EPF

No

12%*(BP+SA)

2,172

Employer ESI

No

3.25%*(BP+SA)

588

Employer LWF

No

20

CTC

38,780

CTC (Annual)

4,65,360

In the above example, the Included Components (=Wages) sum as: 15,000 + 3100 = 18,100/- which is 50.3% of the Gross Pay.

Hey, you talked about Flexi Benefits. What’s it?

Flexi benefits is a way for providing income tax exemption benefits for your employees. There are certain salary components that the Government of India allows employees to save taxes on. The idea is to allow, at the start of the financial year, employees to choose these benefits if they want them. Employer may then exclude those components from TDS and at the end of the financial year, the employees shall submit the proofs to the employer who may then re-calculate the taxes based on the quantum of proofs. Some such components are:

HRA: HRA up to 40% of the Basic pay in non-metro cities and 50% of basic pay in metro-cities is exempt from income tax (subject to certain other conditions therein)

Food Coupons: Differs for industry and days of work, but in general Rs. 2500/- per month is exempted when provided as food coupons/food cards (not as cash).

Annual Gift Coupons: A sum up to Rs. 5000/- per year if provided as a gift coupon is exempted from income tax.

Telephone and Internet: The cost of internet and telephone, against bill submissions, are exempted from income tax. You may keep a logical limit as Rs. 2500/- per month for the same.

Books & Periodical: same as Telephone and Internet.

Fuel and Vehicle Maintenance: Rs. 1800 to Rs. 2400/- per month depending on the CC of the engine, and only available for Cars. Usually provided to senior leaders or those who may undertake travels on behalf the company.

It may also be noted that if the company otherwise reimburses any of the above components, the same shall not be duplicated as a salary component.

In the interest of controlling the Wages, you may want to revisit if you should be offering all of these flexi benefit components at your organisation. If some employees do not opt for these, their Special Allowance may increase and hence the Wages. Have a look and decide for yourself!

Can we restrict the EPF to Rs. 1800/- per month?

Rs. 1800/-, which is the 12% of the statutory limit of Rs. 15,000/- per month is the mandatory (upper cap) payment to EPF. Any amount above this is voluntary. If the organisation decides to cap the EPF at Rs. 1800/- per month, they are at their will to do so. But if the organisation has provided a higher figure in the offer letter/appointment letter, they will not be able to take a one-sided decision of reducing this component. Maybe, you want to revisit your offer letter/appointment letter templates for future issues 🙂

Can’t HRA be more than 40% of Basic Pay?

HRA can. 40% of Basic Pay is the limit for income tax exemptions. Don’t confuse yourself between income taxability and definition of Wages.

How’s it going to affect my take home salary?

If your organisation has included Gratuity as a component in the CTC, then if the Gratuity component goes up and CTC remains the same, it will effectively reduce your take home salary. Similarly, if the CTC is fixed and the employer redesigns the salary structure in such a way that the EPF/ESI component goes up, that will also affect your take home salary. It all depends on how your current salary structure is defined and how it is going to be in Apr 2021. Non-HR readers: you may want to consult your HR team soon!

Disclaimer

This article is written in my personal capacity and advisory in nature. The figures or components mentioned herein have no relationship with my employer or employer’s decisions. Neither my employer nor does my professional role endorses the content in this article. I shall not be liable to any action that you conduct or pursue upon the reading provided by me above.

Well, let’s admit it. At some point in our HR Career, we have all wondered: should we include DA mandatorily in the structure, should we keep the Basic Pay at 30%-40%, or Should CTC include Gratuity? Certainly, I did, especially as I come from an Engineering background with no formal education in HR. The beauty of lack of HR knowledge was that I had to find each of these stuff from scratch for which the web and my fellow HR colleagues from and around Kochi helped. Special thanks to the connections I received through NIPM (one of my imminent blogs is on why HRs should network; catch you there soon!).

In this article, I intend to give a primer—a very basic understanding—of how we can structure the salary in India. I would speak of the structure as of 2021, to the best of my understanding, belief and practice.

Wait, tell me about the parlance!

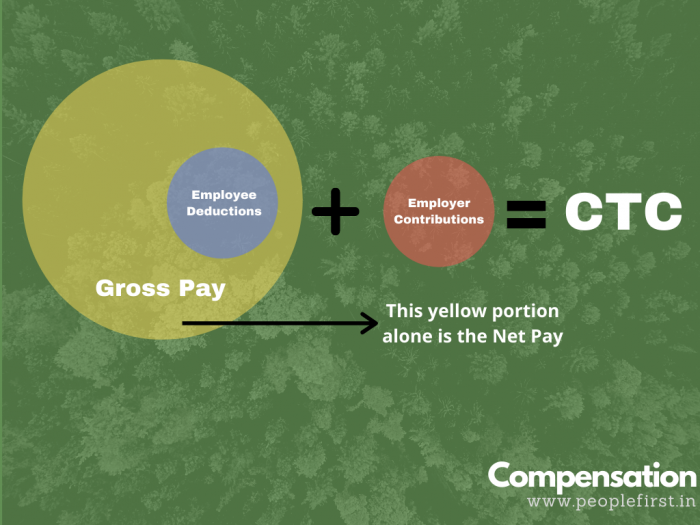

Before we begin, let’s make sure that we get the terms right. During my tenure as an engineer, I never cared about the terms such as Gross Pay and what mattered was the CTC and Cash in Hand. But as an HR professional, there’s more to it and I believe all folks across all departments should get an idea about the payroll parlance. Here’s the gist:

A high-level overview of components of CTC

Cost-to-Company (CTC): This is an accounting term with no legal definition whatsoever. You cannot find this term in any of our labour acts. You use it for your convenience, or for accounting purposes. No one else cares (except probably the job applicants).

Employee/Employer Contributions: There are some mandatory contributions that employee and employer have to make periodically. While employee contributes Employee EPF, Employee ESI, TDS, Professional Tax, Employee Labour Welfare Fund contributions, etc., the employer also needs to make contributions such as Employer EPF, Employer ESI, Employer Labour Welfare Fund contributions. Employee contributions are deducted from the Gross Pay, while Employer contributions are outside the Gross Pay. More on those terms below. Please note that EPF and ESI are mandatory only if your organisation falls into the respective requirements.

Gross Pay: Before I define Gross Pay, we must understand that the CTC is the sum of all payroll expenses an employer incurs on an employee. Basically, CTC includes the salary and other expenses the employer incurs (more on that later). Now, let’s split the CTC as (What Employee Deserves + Extra Expense for the Employer). Here, the “what employee deserves” component is the Gross Pay. Look at the Venn chart above.

Net Pay: An employee has to pay statutory (or even non-statutory) contributions such as EPF, ESI, TDS, etc. These contributions of the employee are deducted from the Gross Pay. In effect, the Net Pay = Gross Pay — Employee Contributions.

Well, we got it covered; pretty much!

It’s important to have the right mixture of components for a tasty meal.

Oh wait, I got your question. You’re basically asking, what all can be there in the ‘Employer Contribution’, correct? Well, the answer is ANYTHING. You can include the mandatory employer contributions as detailed above, plus some other stuff. Some companies include valuation of ESOP in the CTC, some include the amount that the company pays for insurances for the employee/family, etc. As a standard measure, let’s keep the statutory contributions such as ER EPF, ER ESI, ER LWF and the like in the CTC. The best practice, in my opinion, would be NOT to include benefits and other rewards in the CTC with the purpose of inflating it to look attractive. Variables are welcome to be included in the CTC, but we need to mention that they are variables.

How do I structure the Employee Salary?

We’ve finally come to the million dollar question. How do we compartmentalise the salary? I am trying to explain this in the form of a FAQ compilation below:

What are basically the components of Gross Pay?

Broadly, let’s say, Gross Pay contains the Basic Pay, DA, HRA, and other allowances.

Why have you mentioned HRA separately, even when it is an allowance?

HRA has some exemptions with respect to definitions of wages (e.g: EPF calculation where HRA is exempted from consideration).

Okay, understood. Now, tell me whether that DA is mandatory?

As long as you are paying above the minimum wages (read my other article on Minimum Wages to understand how DA is calculated), you can subsume DA in the Gross Pay, without having to show it separately. There are certain occasions (e.g: in the case of those who are using the Wage Protection System in Kerala) some organisations are forced to show DA separately, which I would have no objections against.

How about Basic Pay? Is it 30% or 40%?

Basic Pay used to be defined as any percentage of the Gross Pay by organisations at their will. But as per the proposed Code on Wages, 2019, to be effective from Apr 1, 2021, the (Basic Pay+DA) component should be at least 50% of the Gross Pay (legal nerds, please do not raise your eyebrows; I have used the term ‘should’ as in suggestive parlance and in a practical sense). Assuming that you are not showing DA component in the salary structure, let’s then fix Basic Pay as 50% of the Gross Pay.

Remember, if you are following 30% or 40% of Gross Pay as Basic Pay, you are recommended to revise the same to 50% wef Apr 1, 2021. This will, also, have impact on your financials such as Earned Leave Encashment, Gratuity, etc.

Earmarking the right amounts of the CTC under various heads is not only mandatory but the right thing to do.

Aha, I see. So Basic is Fixed. How about HRA?

HRA is NOT a mandatory allowance. But it is a general practice to provide HRA for the employees to meet their accommodation expenses. Further, HRA is exempt from income tax, while Basic Pay, DA and allowances such as Special Allowance are fully taxable. HRA has an income tax exemption rule, which is three-tiered, details of which I am omitting for now. For metro cities, a maximum of 50% of Basic Pay can be non-taxable, while in non-metro cities, it is 40%. I would then suggest that we go with HRA = 40% of Basic Pay if you are in Kerala.

We’re getting close. Now tell me about ‘Other Allowances’?

Code on Wages mentions about Retaining Allowance, which is an allowance provided to the employee for the retention purposes (this should be part of the offer letter if you are providing it, and you should call it ‘Retaining Allowance’ itself). Generally, new-age companies, usually do not include this in their structure and provide the rest of the salary as “Special Allowance”.

So, in short and in a crude form:

Gross Pay = Basic Pay + HRA + Special (Other) Allowance.

Conveyance allowance is a thing of the past. HRs usually included it in the salary structure since that component, up to an extent, along with Medical Reimbursement used to provide some tax benefits to the employee. Not any longer. It stopped two years ago when the concept of standard deduction was introduced in the union budget and there is no point of mentioning Conveyance Allowance in the pay structure unless you want to have one more column for your Finance team to manage.

(But wait, the Conveyance Allowance may sound well for salary structures when Code on Wages comes into force on Apr 1, 2021. That’s a different subject to talk about; but for starters, look at the exemptions from the definition of ‘wages’)

No, it can’t be this simple. I do not see any other allowance—such as LTA, Books and Periodicals, etc. Where are they?

Now we are on the right track! Well, these allowances are non-mandatory allowances, but at times provide great relief for the employees from a portion of their income tax. Such allowances are in fact reimbursements against actual bills, though some of them are paid in advance under the expectation that the employee would submit the bills to the employer by the end of the financial year.

Now to answer the question, yes there can be some such allowances as part of the salary structure. But they are simply the babies of the ‘Special Allowance’. Special Allowance (even this one is not a mandatory allowance; we use it as a filler bucket to make sure that the components add up to Gross Pay) is fully taxable. One can split the Special Allowance into smaller allowances/reimbursements so that a part of it becomes supposedly non-taxable. That’s a story for another discussion, which you can see in my next blog—Flexi Benefits as part of Salary Structure.

Okay, but you didn’t tell us about the statutory calculations yet.

Fine. Here’s the snapshot. Tables speak better.

Component

Per Month Contribution

Observation

EE EPF

12% of (Basic Pay+DA+Other allowances excluding HRA)

Go with 12% (Basic + DA + Special Allowance)*Some orgs have been exempted and some have 10% contributing rate

ER EPF

12% of (Basic Pay+DA+Other allowances excluding HRA)

Go with 12% (Basic + DA + Special Allowance)*

EE ESI

0.75% of ESI Wages

ESI wages include all components including Basic Pay, HRA, Special allowance, OT, etc., but excludes components like Annual bonus, Retrenchment compensation, and Encashment of leave and gratuity

ER ESI

3.25% of ESI Wages

Same as above –

PT

Depends on your state and salary range. This will help you

EE LWF

Rs. 20/- for S&CE LWF in Kerala. Differs based on the nature of establishment

ER LWF

Rs. 20/- for S&CE LWF in Kerala. Differs based on the nature of establishment

TDS

On the Employee’s Earnings. Depends on the existing Income Tax rates

One may or may not include this as part of Employer Contributions

Table 2: Statutory Deductions on Salary

* Assumption: No other ordinarily paid allowances (other than those like OT, Performance-based incentive, etc).

Legal deductions are the savings for the retirement of your employees. Help them plan right!

So far so good. But I have read that there is a cap for EPF contributions. What is that and how is it incorporated in the salary structure?

Yes, EPF up to 12% of Rs. 15,000/-, i.e. up to Rs. 1800/- per month by Employee and Employer each is mandatory. If the (Basic + DA + Other allowances except OT, Bonus, HRA, etc.) is less than 15,000/- per month, then the EPF contribution will be less than Rs. 1800/-, which is fine. Suppose the above amount is Rs. 25,000/-. Then the 12% of 25,000 = Rs. 3000/-. The employee is not liable to pay this entire amount to EPF and can decide to cap it as Rs. 1800/-. This would mean that the employee’s EPF deduction will be Rs. 1800/- instead of Rs. 3000/-, meaning the net salary might increase since the deduction is lesser.

Another catch here is, the employer is liable to pay the equal contribution as the employee makes. So if the employee decides to cap it at Rs. 1800/-, the employer can also do the same, which may be a loss to the employee in the long term as a hole on the savings. But modern-day organisations tend to transfer the benefit of this capping to the employee, by fixing the CTC and increasing the Gross Pay to match the difference, still, all of them totalling to CTC. This would mean that the employee might get a higher net salary even if s/he caps the EPF contribution, but the transfer of benefit depends on the employer and is at their will.

Popular Posts on this Website

The post is getting longer by the minute. Would you like to conclude?

So, in short, our intention is to add up the component to Gross Pay and then add employer contributions to reach the CTC. When an offer is made (or a salary revision is recommended), companies usually look at the total cost that it would incur. The rest is on HR to design the structure in the most favorable manner.

More fun on the way

The calculation to sum up earnings, employer contributions, etc. to reach the CTC is pretty straightforward with simple arithmetic calculations. But it can become slightly complex when you are given a CTC and asked to bifurcate it to various components especially when there is a cyclic dependency is involved (e.g: ESI contribution depends on the components of the salary structure, while those components depend on the ESI contribution).

This is not rocket science and can be solved with a system of first-degree multi-variable equations. As long as we have HRMS in place, this won’t be a headache, but don’t you think it would be fun to go back to high school math and see how that helps in the above HR situations? Post your responses in the comment below and let’s see who gets it right first! Let me blog on the math later.

Salary Structuring may be an operational aspect of Human Resources, but it definitely is an important piece of the job.

I am sure your you were curious as to why the number 17,742/- for a Software Engineer when you clicked on the link to land this article. Let’s see in detail. By the way, if you are a software engineer in Kerala getting paid below this figure, it’s probably the time to send this article to your HR Manager 😉

Context

Recently, on Dec 24, 2020 to be exact, Government of Kerala announced the revised Minimum Wages for the Software industry in the state, after long 10 years of the earlier revision. Numbers have soared up. This article discusses the concept of minimum wages, with examples pertaining to Kerala state; however, the concept should be the same throughout the country.

What’s this “minimum wages”?

As the name implies, the minimum wages is the minimum wage per month to be given to an employee of a particular sector in a state. There is a national minimum wage declared by the central government, and various state-level minimum wages. The idea is to keep the state-level minimum wages equal to or above the national minimum wages. The concept of minimum wages will ensure access to equitable and justifiable pay, thereby eliminating the chances of exploitation by the management.

When is it decided?

Minimum wages are revised periodically. Minimum wages are defined for each sector separately. For example, the minimum wages for Software sector differs from that for the Oil Mills sector. There are roughly 80 such sectors identified for the State of Kerala; and similar numbers for other states as well. Governments revises the minimum wages when it deems that there is, inter alia, a significant increase in the cost of living over a period of time which is not manageable by a mere increase in Dearness Allowance (DA).

How is minimum wages calculated?

Minimum wage calculation for a role is easy. For example, look at the latest Software industry minimum wages notification for the State of Kerala below (extracted from here).

If you look at the notification, in the Software sector, roles of jobs are categorised into different grades. For instance, an HR Executive is a Group F employee in the industry, while a Software Engineer is a Group E employee. An organisation needs to categorise all their employees into one of these grades (and, if not already done by any means whatsoever before, it would be advisable to communicate the same through an HR letter/notice, through internal HR portals, payslips, etc. to the employee so that they are aware of the same) Let’s take the example of Group E: Software Engineer for illustration purpose.

Popular posts on this website

Demystifying the Minimum Wages Calculation: An Example

If you look at the Group E: Software Engineer, 16520-250-17770-300-19270 is the salary range shown for this role. What does that mean, let’s have a look!

The minimum wage for an employee who is a Software Engineer in an organisation is Rs. 16520. This amount is exclusive of another factor called Dearness Allowance (DA), which we will see about later.

Now, look at the number 250 in the wage structure. What does it signify? The notification says:

For every five years of completed or to be completed service in an establishment or under an employer, an annual increment at the rate next to the pay scale fixed in the new scale of pay shall be paid as service weightage to the employee concerned.

So, if an employee continues to be a Software Engineer under the same organisation/employer, then for every such service year, a minimum pay hike of Rs. 250/-pm should be paid as service weightage. That is, for someone with salary 16520/- as per month salary, and completed one year of service, s/he should get a minimum wage of Rs. 16520 + Rs. 250 = Rs. 16770/- pm during the second year of service. Every year, this figure per month will increase by Rs. 250/- for the first five years. Hence, s/he will have a wage of Rs. 17770/- pm during the fifth year of service. That’s the third number appearing in the pay structure.

Now, one can see a 300 next to 17770 in the pay structure. That means, we’re now done with the first five years and reached Rs. 17770/- pm as minimum wage for this employee. Hence for the next set of 5 years, the minimum wages should be increased for every service year by, not the old 250 but, Rs. 300/-. Hence, on the sixth year of service, the employee should have a minimum wage of Rs. 17770 + Rs. 300 = Rs. 18070/-. This will continue for the second block of 5 years. Hence, at the end of the 10th year (i.e. the fifth year of the second block), the employee should be getting a minimum of Rs. 19270/- pm as the salary. After the 10th year, the mandatory pay hike stops. If the employee gets promoted to a higher Grade, that’s a different story, in which case the minimum wages for that role will be applicable.

Good for them. The minimum wages talks about the minimum wages to be given, and the minimum pay hike to be given for every service years. If your pay is already above this level, then the employer is NOT obliged to give you the 250 or 300 pay hike.

Now, tell me about DA calculation?

Dearness Allowance is calculated based on an index called Consumer Price Index (CPI). I will skip the economy part and would encapsulate that it is a statistical number published by Dept of Economics and Statistics for various cities in the state, and it depicts the fluctuating cost of living. They publish it here.

DA is a mechanism provided to adjust the salaries for change in CPIs. If you look at the Minimum Wages notification, it says:

In addition to the basic rate of wages, all the employees shall be eligible for Dearness Allowance calculated on the basis of the Consumer Price Index published for the concerned District Head Quarters of the Department of Economics and Statistics at the rate of ₹ 26 (Rupees Twenty Six only) for monthly waged employees and ₹1 (Rupee One only) for daily waged employees respectively, for every point in excess of 300 points of the latest Consumer Price Index Number in the series 1998-99=100.

There are five parts to it:

DA varies for each city (read district HQ)

The rate of DA is Rs. 26/- for monthly waged employees

DA is calculated for every point in excess of 300 points

CPI is published periodically

DA for this sector is calculated basis the CPI in the Series: 1998-99=100.

With these reading in mind, let’s calculate the DA for an employee posted in Trivandrum. Look at the CPI page on the EcoStat website and choose the latest month for which CPI is available. As I write this, it is Nov 2020. If you look at the Trivandrum’s CPI value under the column Estimated Indices for Base : 2011-12 = 100 Base : 1998-99 = 100 for Nov 2020, it is 369. That’s our little guy.

Now, we need to find out the DA from this 369. As per the #3 above, DA is calculated on the CPI-300 value. Here, it is 369-300 = 69.

We need to pay Rs. 26/- per month for every point in this 69. That means, the DA per month for an employee posted in Trivandrum is Rs. 26 * 69 = Rs. 1794/-

DA is paid over and top of the above minimum wage. DA may change when CPI changes.

Tip: An organisation need NOT provide DA as a pay structure component. They can subsume DA component in the gross pay and make sure that the gross pay is above the (minimum wages + DA) figure. But it would sound problematic for organisations who use the Wage Protection System, which mandates the DA component as such, in which case one may decide to keep that little guy in the pay structure.

Are we talking about Gross Salary or Basic+DA?

With the introduction of Code on Wages, 2019 (to be in force from Apr 1, 2021), all confusions with respect to the definition of wage will vanish. You may consider the Basic + DA + Other ordinarily paid allowances (other than OT, commissions, performance-based incentive, etc.) as the wage for this purpose, meaning we’re talking about the Gross Pay. Confused about Gross Pay, CTC, etc.? I’ll write about it in my next article 😉

Compliance is a Culture.

When is this to be effective from?

This notification is to be effective from Dec 18, 2020. Even if December 2020 and/or January 2021 salaries are already paid out by the employer, they are to abide by these changes. If there are revisions to be made as per this notification, then employers have to comply and give arrears wef Dec 18, 2020.

For the existing employees, if the salaries are to be revised to comply with this notification, then the employer must take care of the service weightage as well.

Where can I see minimum wages for other sectors?

Govt of Kerala published minimum wages notifications on this page. This is the old notification for the Software Industry.

An exercise

Well, now find out the minimum wages to be paid to a Senior Software Engineer with 3.2 years of experience in the current organisation in that grade, and posted at Calicut. Post your answers in the comment box and let’s see how many of you get it right 😉