Accepting an invitation from the Placement Cell of XIME Kochi, I, along with six other HR professionals, conducted mock interviews with the 2025 MBA batch on September 20, 2025. Each of the HR professionals was allotted 9-10 students, and the interviews spanned around 3.5 hours in total. We gave individual feedback to students in respective panels, post which all students and panellists gathered, where the HRs shared their wisdom.

I shared a few pieces of instructions. A couple of students approached me after the session, asking if I could write down what I had spoken about or create a video on it. Hence, this article.

Interactive Session after the Mock Interviews on Sep 20, 2025 at XIME Kochi

To those experienced professionals: there is nothing new in here. This is just basic wisdom and hence scroll away.

To fresh grads: there is nothing in this article that is not available on the web. But in case this helps you be better candidates, that’s gratifying to me.

Research the organisation thoroughly

Read the company’s website and recent news.

Understand competitors and industry trends.

Look for past interview experiences online (LinkedIn, Glassdoor, etc.).

Analyse the Job Description

Break it into required skills, responsibilities, and behavioural traits. Use ChatGPT or similar tools extensively for this purpose.

Map your college projects, internships, school/college event management or club activities, and skills to these requirements. Leadership experience, if any, write it first.

Prepare responses showing how you fit the role.

Master your resume

Be ready to explain every point on the resume in detail. Expect a drill-down of whatever you have written on the resume.

Prepare for Behavioural Event Interviews (BEI)

Research the potential behavioural competencies for the role you have applied for.

Use the STAR method (Situation, Task, Action, Result) approach in your responses

Keep answers structured and concise (1–2 minutes max). Do not talk forever; the interviewer may lose interest or lose track.

Prepare at least 5–6 STAR stories covering the behavioural competencies for the role, from your personal life, school/college life, and internship stint.

Some common (not exhaustive) competencies for entry-level roles are:

Teamwork and collaboration

Conflict resolution

Leadership and initiatives during school/college

Handling failures

Problem-solving under pressure

Achieving results with limited resources

Build a strong LinkedIn profile (7-star checklist) + Connect/Network with the right people

Professional profile picture. No selfies, please.

Headline aligned with your career goals

Customised vanity URL (linkedin.com/in/yourname)

Strong “About” section with career goals + skills

Internship experience listed with bullet points and results

Skills endorsed + recommendations from teachers/internship managers

Active engagement: post insights, share/write articles, comment meaningfully. You do not need to perform the cringe LinkedIn actions to be visible.

Highlight the most relevant experiences based on the JD.

Keep it concise: ideally 1 page. In PDF, unless specified. Name the file appropriately.

Use a professional email ID (ir0ckbutImbad@gmail.com is a no-no)

Start with a Summary at the top, rather than a Career Objective. The summary should give an idea of your background to the interviewer in less than 5 sentences. This is, also your selling pitch.

Include LinkedIn URL and any other portfolio URLs at the top of the resume

Customise your resume for the JD (do not lie, though). Use ChatGPT or similar tools to understand the keywords in a JD and use the relevant (and what you actually have) in your resume.

There are a zillion videos on YouTube that tell you how to prepare a resume properly. I personally recommend videos by Jeff Su, or Ali Abdaal. Watch their videos on resume writing, creating LinkedIn profiles, networking, and more.

Include a cover letter only if specifically asked for.

Prepare for common HR questions

Why MBA/BTech/whatever your course is? Why your specialisation/this role/organisation?

Career goals (short-term and long-term).

“Tell me about yourself” in 60 seconds. This is your elevator pitch to sell yourself. Do not waste this opportunity. Do not spend time on irrelevant details about you during this time.

Get ready to ask questions at the end

Prepare 1-2 thoughtful questions for the interviewer. This need not always be about the salary or location of the job.

Example: How does this role contribute to the company’s strategy?

Practice interview delivery

Speak clearly, avoid filler words to the extent possible (umm, like). You will need to practise this; it is not an overnight success that you can achieve.

Maintain eye contact, upright posture, and a positive tone. Dress for the occasion.

Listen carefully before answering. You can take time to think (Steve Jobs style!)

Admit honestly if you don’t know something, but show willingness to learn. And be genuine.

Sick Leaves: Up to 12 days in a calendar. It can be less than 12 as well. Maximum 12 is defined in S&CE Act. Lapses on Dec 31 if unused.

Casual Leaves: Up to 12 days in a calendar. It can be less than 12 as well. Maximum 12 is defined in S&CE Act. Lapses on Dec 31 if unused.

Earned (Annual) Leave: 1 day per one month of service. It can be credited as 12 days when someone completes 1 year of service, and then every 30 days, 1 day should be additionally credited. You can also give 1 day/30 days from the beginning as well without having to wait for someone to complete 1 year of service. This is the only leave that is carried forward to the next calendar year. A minimum of 24 days should be allowed to be carried forward (though it can accrue, i.e. go beyond 24 within the calendar year). If someone has more than 24 days of Earned Leave balance on Dec 31, only 24 need to be carried forward to the next year. Companies can, at their discretion, increase this limit to 36, 48 or even more. At the time of exit, this leave balance should be paid to the employee in the full and final settlement (and it is tax-free up to 25 Lakhs). You can pay (per day basic pay * leave balance) for encashment. To arrive at the per day basic pay, you can divide the monthly basic pay by 26.

Holidays: 4 mandatory national holidays (Jan 26, May 1, Aug 15, and Oct 2) + 9 festival or regional holidays = 13 days. If a mandatory holiday falls on a weekend, companies usually give an additional holiday to keep the total holidays as 13 in a calendar year. Companies can decide to allow more holidays. For the 9 festival holidays, companies can provide a larger list of holidays and call them restricted holidays (thereby allowing employees to choose 9 holidays of their liking, totalling the holidays to at least 13).

Maternity Leave: 182 days of paid Leave. This is as per the MB Act.

Sterilisation Leave (for vasectomy and the like): 6 days for men, 14 days for women and it is also a paid leave.

Abortion/Miscarriage Leave: 6 weeks of paid leave.

Paternity Leave: Not mandatory. Companies usually give 1-2 weeks of paid leave.

[Download the checklist at the end of this article]

Are you looking for a payroll (managed) partner in India? It can be overwhelming as to what aspects to be mindful of in the process.

Here is a set of questions that you can consider to ask the vendors you have shortlisted. Not all of these questions may be applicable to all organisations and not all questions are on this document either.

Below are some abstract set of questions and a detailed set of questions are provided at the end of this article for you to download.

Input and Output

Starting with how the input-output communications occur, their cadence, mode of communication, how results are presented, availability of various reports, pay structuring and support for pay components, monthly or year-end TDS process, etc. can be points of discussion. How about new joiners and leavers?

Admin

Whether the partner allows admin access to the payroll platform to select employees of the client organisation, what kind of reports can be generated by the admin, etc. can be thought of before taking a decision.

ESS

Will employees get access to an Employee Self-Service portal where they can see their pay details, and tax calculations, declare investments, download payslips, submit reimbursements and year-end proofs, etc.? Well, this is important for employee experience and should be considered as a serious point of discussion. Questions like whether there is a mobile app for the ESS is also good question to ask.

Payslips

How customisable are the payslip structure and formats? Can the client organisation’s branding guidelines be followed? What information (such as PF#, UAN, LWF#, PAN, Bank Account#, etc.) can be shown on the payslip?

Integration

Can the payroll partner integrate their tool into the client organisation’s HRIS? How about various documents such as Payslips, Form 16, etc.? Will they appear on the HRIS as well? How about compensation analytics and tax projections?

Compliances

Can the payroll partner take care of EPF/ESI/PT/LWF payments, returns, etc.? How about the other labour law returns/forms to be kept/registrations to be taken? Or, will the client organisation have to engage another service provider for these services?

Today, Jul 27, marks my another work anniversary in the HR function, and the anniversary of my first day at Profoundis—later acquired by FullContact, Inc. I am trying to reflect on some great people matters our leadership and HR teams are proud to have envisaged and implemented over the last few years, besides the usual HR business stuff. Not in order of occurrence, though. The credit goes to our awesome leadership and HR teams across offices of FullContact 🙂

What led us to these decisions/benefits

FullContact takes decisions based on the Core Values it is built on. Our people decisions are mostly based on treating people as independent adults and believing in an accountability-driven organisation than a task-driven organisation. Leaders of our organisation have shown immaculate allegiance to these two principles while making people decisions. What if it goes wrong has always been part of the decision-making process, but has not been the deciding factor that prevented us from doing something right.

FullContact India got GPTW Certified within 2.5 years of its operation

FullContact India got recognised as a Great Place to Work®

Within 2.5 years of beginning its operations, in 2019, the FullContact India office was recognised as Great Place to Work Certified®. This reflected how our members felt about the organisation as a great place to be at, how our processes aligned to benchmarks that the GPTW team set. We were one of the very few SME IT organisations, back then, to achieve GPTW certification back then in Kerala.

FullContact does not ask for payslips from previous organisations

Travel Benefits

FullContact used to offer travel benefits (then called PAID Paid Vacation) that offers both two weeks of paid leave just for travel and a sum of Rs. 1,50,000/- per year to take an actual vacation. Later this was revamped to be called FULLBalance Vacation Benefit with UNLIMITED paid vacation time and a sum up to Rs. 2,15,000/- per year to take the vacation. At the latest, I recently took a trip to Turkey and Azerbaijan, thanks to this policy.

Holidays

FullContact has an unparalleled holiday and leave policy in India among the IT SME organisations of our nature. As I write this, FullContact India employees enjoy double the national average per year as holidays—27 in total in a year. This includes 13 scheduled holidays as per norms in the Holidays Act, ½ Day Fridays during Jul-Sep, and year-end holidays from Dec 26-31. As part of our ½ Day Fridays policy, all the Fridays from Jul 1—Sep 2 are half-day Fridays, meaning we close our work by noon on Fridays and take an early weekend to spend more time with ourselves and our beloved ones.

FullContact offers unparalleled vacation benefits and holiday plans

An extended Leave Policy

FullContact has always tried to maintain a top-notch leave policy. Apart from the typical Sick/Casual/Earned/Maternity/Miscarriage/Abortion/Adoption/Sterilisation leaves, FullContact India also offers:

Unlimited Hospitalisation paid leave, for as long as the employees remain in a hospital; this is not to be availed from sick leave or any other bucket

Paternity paid leave for 21 days

Bereavement paid leave for 14 days

Family First paid leave for 3 days to spend time with family for any reason (e.g: celebrating birthdays, anniversaries, just spending time, etc.)

No-leave-approval process

Effective Jan 1, 2022, FullContact India moved from Leave Approvals to Leave Acknowledgements. This means, our paid leave requests are auto-approved and only an acknowledgement will be sent to the reporting managers as FYI. There’s no approval process if Earned Leaves and Casual Leaves are applied for at least 5 calendar days in advance. All Sick, Covid, Hospitalisation leaves, and Bereavement and other sickness/illness-related leaves are auto-approved without any notice requirement.

Unlimited VTO

FullContact, besides our leave policy and holidays, offers UNLIMITED Paid vacation time off for all our members. Our members are able to take any number of days as vacation, besides all the short-term statutory leaves and holidays! We have a formal policy to encourage members to take a MINIMUM of three weeks of vacation per year. The new Unlimited Vacation policy takes care of the other end of the benefit, making it practically and technically unlimited.

FullContact offers unlimited paid vacation time off for all members

Health Insurance for family and parents fully paid for by FullContact

Accidental Insurance fully paid for by FullContact

Life Insurance fully paid for by FullContact

Employee Access Program fully paid for by FullContact

Equipment reimbursement for people of determination

ESOPs

FULLBalance Vacation Bonus

Monthly work-from-home reimbursement

Home office setup cost reimbursement

ThankFULL Rewards and Recognition Program

SkillFULL Employee Training Program

SuccessFULL Career Pathing Program

And we are default work remote 🙂

First among the few to close down physical offices when the pandemic hit

I included this in the list since I am proud of the leadership team that unanimously decided to shut down our physical office space until things get back to normal (phew, it took two years for it to be normal) when Covid 19 hit. We were one of the first few offices to go remote—and we went fully remote, permanently so later—when the pandemic hit. Our flexible work policy dueing pre-Covid era that empowered our members to work from home did help us in making this transition with ease.

The guiding light for decision-making was of course the safety and wellbeing of our members. We were also one among the first very few SME IT orgs in the state who incorporated a home office setup cost reimbursement upto Rs. 7500/- which was later increased to Rs. 10,000/-. We also offered (and continue to offer an increased amount of) Rs. 1000/- per month toward home expenses such as the internet charges.

Unparalleled Covid 19 Benefits

Our organisation, like many others, took the decision to stand by our members during the tough times of Covid 19. We released a stream of Covid Benefits for our members and their families. It included sponsoring covid vaccinations for members, spouse, kids, parents and parents-in-law and our members appreciated this benefit.

Other Covid 19 benefits included 14 days of paid time off if a member is Covid positive, Covid insurance for all employees if not already covered by the organisation’s group health insurance, employee access program to provide mental support and counselling sessions free of cost—for members and their families, 7 days of paid time off as Caregiver PTO to take care of a family member in case of being Covid positive, two days of additional paid leave for vaccination, salary advance for members affected by Covid, reimbursement of Covid tests, and continuation of salary for six more months in case of an unfortunate Covid death. We also ran the #HealthyFullContact initiative and also put together some Mental Health and Wellness Ideas that our members found useful.

FullContact offered unparalleled Covid 19 benefits to our members

An Inclusive workplace

Developing an inclusive, equitable and diverse workplace has always been one of our prime agendas—though this is a work-in-progress. Our DEI teams across both offices set SMART Goals and work toward making them a reality. This is a picture that our team treasures and gender inclusivity of this magnitude is something that we enjoy having at FullContact. We also offer reimbursement of the cost of equipment used by our members who are people of determination, up to 7500/- in a year.

Compensation Structure with Flexi Benefit Plans

FullContact introduced Flexi Benefit plans to make sure that our employees get to decide, to an extent, how their compensation should be structured. We made sure that we do not inflate CTC for the sake of making it bigger by including components like medical insurance premiums, gratuity, variable bonus, ESOPs, etc. in the CTC—the philosophy was to keep it simple for the employees and prospective employees to give an idea about a fixed compensation.

There’s so much fuss about the new Code on Wages implementation and how to restructure the compensation to be compliant. While the general guideline is to have at least 50% of the salary as Basic Pay, what if you do not keep it so?

Well, while it is recommended that you keep 50% of the total pay as Basic Pay, even if you do not keep it that way, it should not bother you much. In cases where Basic Pay is less than 50%, then the Basic Pay for calculation of other benefits (such as leave encashments, Gratuity, etc.) should be based on the 50% of the salary. This would mean, effectively, allowances cannot be more than 50%, technically or practically—even if you do not restructure the compensation.

However, with that preface, let’s look at some salary structures that one can probably include while making an offer to a prospective candidate (beware: if you are making changes to an existing employee’s compensation, there are things to be careful about) so that there are tax-efficient components:

Tax-avoidance or tax-escaping is not the way; but tax-efficiency is the one.

House Rent Allowance is IT-exempt subject to the Income Tax rules, upto 40% of the Basic Pay in non-metro cities and up to 50% of the Basic Pay (+DA) in Metro Cities. The exact amount of exemption is the minimum of the following three (though you are welcome to have an even higher amount being shown as HRA in the salary structure, it won’t have any impact on the tax exemption):

a) Actual HRA received from employer (that is shown on the payslip) b) 40% or 50% of Basic Pay (+DA) depending on the nature of the city c) Actual rent paid minus 10% of Basic Salary (+DA)

Leave Travel Allowance is IT-exempt subject to the Income Tax rules, and subject to production of proofs as mandated by the Income Tax department. For the exemption to be effective, the payslip should have a component “LTA”. There is no specified limit on the % of LTA, but typically companies follow 5%-8.33% of Basic Pay (+DA) as the LTA amount. List of accepted expenses as LTA proof; note that LTA exemptions are not financial-year based, but based on a block of four calendar years (current block year: 2022-25).

Books & Periodicals Reimbursements: Companies are welcome to include this as a reimbursement component of their total compensation and show it on payslips. They are welcome to provide reimbursement for the books and periodicals that are pertinent to the nature of jobs of the employees, against submission of relevant proofs. While there are no specified limits on this, companies usually tend to keep it in the range of Rs. 1000—2500 per month; senior professionals may be given a higher amount of reimbursement depending up on their role.

Telephone & Internet Reimbursements: Similar on the lines of Books & Periodicals Reimbursements

Fuel and Vehicle MaintenanceReimbursements: This is typically provided to senior leaders in companies, who may have to utilise their cars for business-related intents. Up to Rs. 2400/- per month against proper records of travels and fuel/maintenance receipts.

Professional Development Allowance: Companies can reimburse the cost of courses/training/certification/professional memberships whose expenses are met from the pocket of the employee, against sufficient proofs. Such expenses could be mandated to be directly related to their role at the organistaion and have sane guidelines for which expenses can be considered.

Annual Gift Voucher: Digital or physical gift coupons to the tune of Rs. 5000/- can be given to employees per a financial year, which is income tax-exempt. No proofs are usually required.

Food Coupons: they can be paid in the form of physical or digital coupons/card and are exempt from Income Tax (usually not paid through payroll since cash as such is not being disbursed). No proofs are usually required. Maximum limit per month: Rs. 2500/- depending on the number of days your office operates.

Children Education Allowance: Upto Rs. 100/- per month per child (for a maximum of 2 children per employee) is tax exempt under this category. This benefit can be provided for employees with children only. This does NOT limit employee’s 80C exemption of Children’s Tuition Fees.

Hostel Expenditure Allowance: Up to Rs. 300/- per month per child (for a maximum of 2 children per employee) is tax-exempt under this category.

Uniform Allowance: Applicable if there is a uniform at work.

Include employee/employer contributions such as Corporate NPS

Other means of executive compensation: Executive compensations are another realm, which may include more “benefits” than in the form of “pay components” and hence not delving into those areas now.

Slicing the total compensation at the right measures is the key to a tax-efficient salary structure

Word of caution: While designing the salary structure, the intent should NOT be tax avoidance or tax evasion, but utilising the existing legal provisions to form a tax-efficient structure. In the cases where it is mentioned above that proofs are required, you are still welcome to disburse that part of compensation if the employees do not have proof, but that will attract income tax.

A sample salary structure is provided below (not all of them could apply to you or to a specific employee), for illustration purposes only. Consult your legal team before you implement.

Component

Amount per month

Amount per year

Basic Pay

₹40,000

₹480,000

HRA

₹16,000

₹192,000

LTA

₹3,332

₹39,984

Internet and Telephone Reim

₹1,000

₹12,000

Books and Periodicals Reim

₹1,000

₹12,000

Fuel and Vehicle Maintenance Reim

₹2,400

₹28,800

Professional Development Reim

₹2,000

₹24,000

Food Coupons

₹2,500

₹30,000

Annual Gift Coupon

₹0

₹5,000

Children Education Allowance

₹100

₹1,200

Hostel Expenditure Allowance

₹300

₹3,600

Special Allowance

₹10,951

₹131,412

Gross Salary

₹959,996

Employer Contributions

Employer Contribution to EPF

₹4,800

₹57,600

Employer Contribution to LWF

₹20.00

₹240.00

Employer Contribution to NPS

₹4,000.00

₹48,000.00

Cost to Company (CTC)

₹1,065,836

Tax-efficient Salary Structuring: An Example

Here’s the excel sheet with the above salary structure, for download.

Disclaimer: The views in this article are provided personal and for academic purposes only. They need not reflect the views of my employer/previous employer(s).

“It comes with experience. I can tell if a candidate is hireable within the first ten seconds of my interaction”, I heard a senior HR professional say this three years ago when I was eavesdropping at the break time of an HR conference in Hyderabad. I was still fresh on the job, with hardly one year of experience, and I wished if I could be like him one day.

Fast forward to 2021. I couldn’t still be like him. I read a few human behaviour books in the interim, read about body languages, did a formal course on BEI and watched some TED/TEDx videos on the subject since interviewing is one of my favourite things to do. As yet, that’s a dream not come true, and I wish it stays that way.

Back in college days

I come from the middle part of Kerala state and went to undergrad college in a nearby district. I was a hosteler where we had inmates from all across the state. Those who know Malayalam would know that the way Malayalam is spoken differs almost every 100km within the state. I had a friend from Malabar region whom I heard, on the first day on phone, speaking to his mom, “Ningal evide poyathanu?” (verbatim: Where did you go?). The word ‘ningal‘ (=you) is treated as a word without respect, except probably in a formal setting, in my area of living. One would easily get offended if I would use that word.

I was assuming that my friend was angry with his mom and I did ask him if everything was alright. To my surprise, he was all cool. When probed, he told me that it is common to use that word, without any lack of respect, in the Malabar region. That was sort of a cultural shock for me. The life thereafter was full of such cultural shocks, different ideas, fighting over ideologies, settling for compromise, understanding that people would have different opinions and that the world is no binary. That understanding, maybe, comes with age and experience.

Each candidate is a story book that’s not to beread in 10 seconds.

Then why?

Every person’s story is different. Very unique in every aspect. We know our story. We may know a few others’ stories as well. That does not mean that we know every story. Humans have a tendency to look for patterns in everything they pursue. We are like a machine learning algorithm where there are preset stories (knowledge so far) which we try to match with the new entrant. Unless and until we have sufficient data to classify the new entrant, the algorithm will fail. That classification is the learning process, which needs sufficient data to process.

Hence it is very important that we provide sufficient time hearing people out. This is the only basic step to remove our own biases in the evaluation processes. We need to hear people out. We should look for what they have done in the past, and most importantly why they have done those, and try to extrapolate it to what can be done. This process takes time and this is why I don’t digest when one says they can assess if a candidate is worth hiring in the first 10 seconds itself!

Interviewer is not a machine, nor is the candidate

Both are humans. Even the most learned machines need at least a dozen inputs to identify patterns for an evaluation. Then how can a human being, with their very limited knowledge—howsoever big one would assume it to be—understand a candidate in a few seconds? That would mostly be a biased opinion, I may think.

As both the candidate and the interviewer are not machines, we need to listen. A candidate may be late to the interview, they may have dirt on their dress, their language may not be perfect, their hair may not be combed, they may have had a gap in their career—how would one know what’s the story behind it without them telling us? What if they have a story that will justify these? If an interviewer is suddenly decides on the hirability of a candidate, that’s way too unjustifiable for the very same reason.

Way forward

Tech interviewers may have a different reason to identify if a candidate is suitable for a role faster, but HR interviewers should spend sufficient time to listen to stories of the people. Candidates are adults with a totally different life story than ours. This is exactly why some great companies have thorough and sufficiently long interview practices, even if the candidate may possibly seem a bit off in the first few minutes. HR interviewer’s responsibility lies in traversing through the story to see if there is a new story the candidate can build at your company. Past predicts the future and history is not a subject learnt in 10 seconds.

Much has been said and written about National Pension System (NPS) already. The intention of this article is to give a quick idea to my fellow HRs in the network as to why this is a great benefit you can offer to your employees. Non-HR folks reading this—check with your HR team to see if this is an option at your organisation if you don’t already have it.

What is NPS?

As the name suggests, it is National Pension System. The Govt. of India introduced it for the central and government employees but a few years ago it was extended for the Private Sector employees (and for any citizen of age 15-65, for that matter irrespective of whether they are employed) as well. It is a voluntary pension fund (+wealth creation fund, I might add). Employees can contribute amounts to the NPS fund which will be invested in equity stocks, government bonds, corporate debts, etc.

When does the pension start?

At the time of maturity, one can withdraw up to 60% of the lumpsum. The balance 40% should be invested in annuity (pension), which will be used to give you pension for the rest of your life. One has an option to put in any percentage above 60% up to 100% to the annuity, too. Here’s an NPS calculator.

Can you tell me a little bit more about NPS?

I will skip that part since numerous websites have already written about it—NPS Trust’s website or Wikipedia can be a starter. There are many youtube videos on the topic too. You should be able to read/watch pros and cons of the scheme.

Each bit that you save now will keep your golden years safer

How are the returns?

Better than EPF in terms of absolute profit from invested corpus, from the stats. Dig in here and here’s Scheme E’s returns. The minimum contribution in a financial year to keep the account active is Rs. 1000/-.

How can I join NPS?

Simple. Join here online. Keep digital copies of your PAN, Photograph, Aadhaar and cancelled cheque/bank account passbook with you. The cancelled cheque/bank account passbook should bear your name.

Is contribution to NPS tax-exempt?

Yes, it is exempt in your 80C (and 80CCC, 80CCD(1)). Plus, there is a special exemption of Rs. 50,000/- for NPS contributions under 80CCD(1B). Contributions to NPS is Exempt-Exempt-Exempt, i.e. tax-exempt at the tie of contribution, tax-exempt on the profit earned on an investment, and tax-exempt at the time of maturity (conditions apply).

Well, is it fully tax-exempt?

Your investment is fully tax-exempt at the time of investment. Your return every year that is being added back to NPS corpus is tax-exempt. Your corpus is, well, hmm… two things: exempt for the part that goes to annuity and the rest (that you withdraw) is not exempt. One cannot say that NPS is fully non-taxable at the time of maturity in that sense.

Now tell me, how’s NPS and Corporate NPS different?

Corporate NPS is NPS whose contributions are made through the employer. Instead of you making direct contribution to your NPS fund, you ask your employer to deduct a certain amount from your CTC and contribute to your NPS.

What’s the advantage of having Corporate NPS?

Contributions made through Corporates are tax-exempt under 80CCD(2) for up to 10% of Basic Pay of the employee. That is, if your annual basic pay is Rs. 10 Lakhs, then a contribution up to Rs. 1 Lakh per year is fully tax-free. This is over and above your 80C, 80CCC, 80CCD(1) and 80CCD(1B). Meaning, you still can invest into NPS on your own as per the above sections and claim those tax-exemptions as well, besides the corporate contributions made.

That’s exciting. How can corporates register for Corporate NPS?

Corporates will have to find a PFM and POP. Ask your HR or Finance team to reach out to them and the rest of the onboarding will be taken care of by them. It will need very minimal involvement by your HR/Finance team. Make sure that you choose the PFMs after due diligence (look at peer feedbacks, return rates, etc.).

NPS is one way of saving money for your retirement.

How can we connect employees NPS ID to our corporate NPS?

You should ask employees to provide their NPS (the same NPS ID—known as PRAN—created for their direct investment shall be used for Corporate NPS contributions as well). Provide these PRANs to your PFM and they will link it to your corporate account.

How does this play with salary structuring?

Corporate NPS contributions usually form part of the employer contributions of the CTC. If your offer/appointment letter allows flexibility of revising the salary structure (perhaps at the request of the employee), this is a great benefit to add. You may even offer a choice for the employee to choose an amount up to 10% of their monthly basic pay to be contributed every month (going above 10% won’t be beneficial in terms of tax-exemption). You may also consider providing this as an additional benefit to the existing employer contributions, if the company financials are good, thereby not touching the gross pay.

If Corporate NPS cannot be offered to your current employees owing to a rigid offer/appointment letter, consider offering this as a choosable perk to future employees. They will love it when they see the returns plus the taxes being saved.

Hey, I see options like Aggressive (LC75), LC50 and such. What are they?

These options indicate how aggressive the investments are. LC75, for example, says 75% of the contributions will be invested in equity, while the balance will be in government bonds/corporate debt funds. LC50 would mean and 50% contribution to equity funds. Though corporates can set the nature of aggressiveness at the start of the Corporate NPS, employees will have an option to set their own aggressiveness (and can even change the PFMs for their own fund) after a stipulated time (~1 year).

If your workforce is generally young, say less than 35 years of age, LC75 would not hurt much. If your workforce is comparatively older, say above 40, it’s safe to stay with less-riskier options such as LC50.

What are the cons of NPS?

There could be multiple legs: NPS is a market-linked product and hence the market fluctuations can affect your returns. You will still need to manage your PMS once in a while to make sure that you have higher/steady returns — this needs manual intervention from the investor. Plus, the government still require the investor to keep at least 40% of the maturity corpus to be invested in annuity, whose returns are not at par with the inflation. More here.

This article is also published on LinkedIn and Medium.

Well, let’s admit it. At some point in our HR Career, we have all wondered: should we include DA mandatorily in the structure, should we keep the Basic Pay at 30%-40%, or Should CTC include Gratuity? Certainly, I did, especially as I come from an Engineering background with no formal education in HR. The beauty of lack of HR knowledge was that I had to find each of these stuff from scratch for which the web and my fellow HR colleagues from and around Kochi helped. Special thanks to the connections I received through NIPM (one of my imminent blogs is on why HRs should network; catch you there soon!).

In this article, I intend to give a primer—a very basic understanding—of how we can structure the salary in India. I would speak of the structure as of 2021, to the best of my understanding, belief and practice.

Wait, tell me about the parlance!

Before we begin, let’s make sure that we get the terms right. During my tenure as an engineer, I never cared about the terms such as Gross Pay and what mattered was the CTC and Cash in Hand. But as an HR professional, there’s more to it and I believe all folks across all departments should get an idea about the payroll parlance. Here’s the gist:

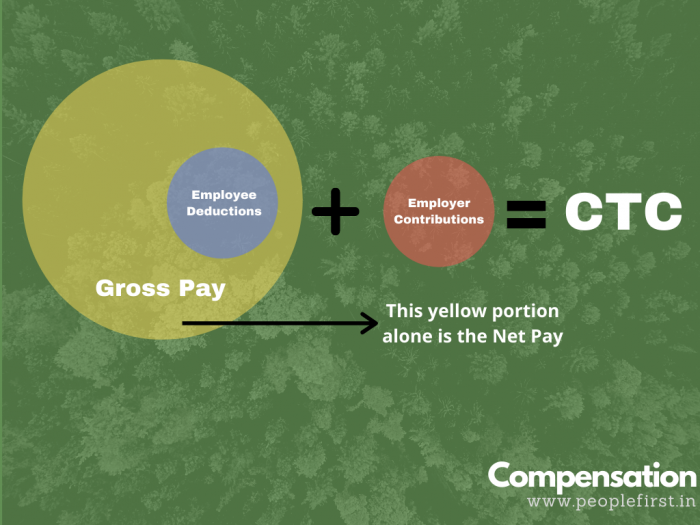

A high-level overview of components of CTC

Cost-to-Company (CTC): This is an accounting term with no legal definition whatsoever. You cannot find this term in any of our labour acts. You use it for your convenience, or for accounting purposes. No one else cares (except probably the job applicants).

Employee/Employer Contributions: There are some mandatory contributions that employee and employer have to make periodically. While employee contributes Employee EPF, Employee ESI, TDS, Professional Tax, Employee Labour Welfare Fund contributions, etc., the employer also needs to make contributions such as Employer EPF, Employer ESI, Employer Labour Welfare Fund contributions. Employee contributions are deducted from the Gross Pay, while Employer contributions are outside the Gross Pay. More on those terms below. Please note that EPF and ESI are mandatory only if your organisation falls into the respective requirements.

Gross Pay: Before I define Gross Pay, we must understand that the CTC is the sum of all payroll expenses an employer incurs on an employee. Basically, CTC includes the salary and other expenses the employer incurs (more on that later). Now, let’s split the CTC as (What Employee Deserves + Extra Expense for the Employer). Here, the “what employee deserves” component is the Gross Pay. Look at the Venn chart above.

Net Pay: An employee has to pay statutory (or even non-statutory) contributions such as EPF, ESI, TDS, etc. These contributions of the employee are deducted from the Gross Pay. In effect, the Net Pay = Gross Pay — Employee Contributions.

Well, we got it covered; pretty much!

It’s important to have the right mixture of components for a tasty meal.

Oh wait, I got your question. You’re basically asking, what all can be there in the ‘Employer Contribution’, correct? Well, the answer is ANYTHING. You can include the mandatory employer contributions as detailed above, plus some other stuff. Some companies include valuation of ESOP in the CTC, some include the amount that the company pays for insurances for the employee/family, etc. As a standard measure, let’s keep the statutory contributions such as ER EPF, ER ESI, ER LWF and the like in the CTC. The best practice, in my opinion, would be NOT to include benefits and other rewards in the CTC with the purpose of inflating it to look attractive. Variables are welcome to be included in the CTC, but we need to mention that they are variables.

How do I structure the Employee Salary?

We’ve finally come to the million dollar question. How do we compartmentalise the salary? I am trying to explain this in the form of a FAQ compilation below:

What are basically the components of Gross Pay?

Broadly, let’s say, Gross Pay contains the Basic Pay, DA, HRA, and other allowances.

Why have you mentioned HRA separately, even when it is an allowance?

HRA has some exemptions with respect to definitions of wages (e.g: EPF calculation where HRA is exempted from consideration).

Okay, understood. Now, tell me whether that DA is mandatory?

As long as you are paying above the minimum wages (read my other article on Minimum Wages to understand how DA is calculated), you can subsume DA in the Gross Pay, without having to show it separately. There are certain occasions (e.g: in the case of those who are using the Wage Protection System in Kerala) some organisations are forced to show DA separately, which I would have no objections against.

How about Basic Pay? Is it 30% or 40%?

Basic Pay used to be defined as any percentage of the Gross Pay by organisations at their will. But as per the proposed Code on Wages, 2019, to be effective from Apr 1, 2021, the (Basic Pay+DA) component should be at least 50% of the Gross Pay (legal nerds, please do not raise your eyebrows; I have used the term ‘should’ as in suggestive parlance and in a practical sense). Assuming that you are not showing DA component in the salary structure, let’s then fix Basic Pay as 50% of the Gross Pay.

Remember, if you are following 30% or 40% of Gross Pay as Basic Pay, you are recommended to revise the same to 50% wef Apr 1, 2021. This will, also, have impact on your financials such as Earned Leave Encashment, Gratuity, etc.

Earmarking the right amounts of the CTC under various heads is not only mandatory but the right thing to do.

Aha, I see. So Basic is Fixed. How about HRA?

HRA is NOT a mandatory allowance. But it is a general practice to provide HRA for the employees to meet their accommodation expenses. Further, HRA is exempt from income tax, while Basic Pay, DA and allowances such as Special Allowance are fully taxable. HRA has an income tax exemption rule, which is three-tiered, details of which I am omitting for now. For metro cities, a maximum of 50% of Basic Pay can be non-taxable, while in non-metro cities, it is 40%. I would then suggest that we go with HRA = 40% of Basic Pay if you are in Kerala.

We’re getting close. Now tell me about ‘Other Allowances’?

Code on Wages mentions about Retaining Allowance, which is an allowance provided to the employee for the retention purposes (this should be part of the offer letter if you are providing it, and you should call it ‘Retaining Allowance’ itself). Generally, new-age companies, usually do not include this in their structure and provide the rest of the salary as “Special Allowance”.

So, in short and in a crude form:

Gross Pay = Basic Pay + HRA + Special (Other) Allowance.

Conveyance allowance is a thing of the past. HRs usually included it in the salary structure since that component, up to an extent, along with Medical Reimbursement used to provide some tax benefits to the employee. Not any longer. It stopped two years ago when the concept of standard deduction was introduced in the union budget and there is no point of mentioning Conveyance Allowance in the pay structure unless you want to have one more column for your Finance team to manage.

(But wait, the Conveyance Allowance may sound well for salary structures when Code on Wages comes into force on Apr 1, 2021. That’s a different subject to talk about; but for starters, look at the exemptions from the definition of ‘wages’)

No, it can’t be this simple. I do not see any other allowance—such as LTA, Books and Periodicals, etc. Where are they?

Now we are on the right track! Well, these allowances are non-mandatory allowances, but at times provide great relief for the employees from a portion of their income tax. Such allowances are in fact reimbursements against actual bills, though some of them are paid in advance under the expectation that the employee would submit the bills to the employer by the end of the financial year.

Now to answer the question, yes there can be some such allowances as part of the salary structure. But they are simply the babies of the ‘Special Allowance’. Special Allowance (even this one is not a mandatory allowance; we use it as a filler bucket to make sure that the components add up to Gross Pay) is fully taxable. One can split the Special Allowance into smaller allowances/reimbursements so that a part of it becomes supposedly non-taxable. That’s a story for another discussion, which you can see in my next blog—Flexi Benefits as part of Salary Structure.

Okay, but you didn’t tell us about the statutory calculations yet.

Fine. Here’s the snapshot. Tables speak better.

Component

Per Month Contribution

Observation

EE EPF

12% of (Basic Pay+DA+Other allowances excluding HRA)

Go with 12% (Basic + DA + Special Allowance)*Some orgs have been exempted and some have 10% contributing rate

ER EPF

12% of (Basic Pay+DA+Other allowances excluding HRA)

Go with 12% (Basic + DA + Special Allowance)*

EE ESI

0.75% of ESI Wages

ESI wages include all components including Basic Pay, HRA, Special allowance, OT, etc., but excludes components like Annual bonus, Retrenchment compensation, and Encashment of leave and gratuity

ER ESI

3.25% of ESI Wages

Same as above –

PT

Depends on your state and salary range. This will help you

EE LWF

Rs. 20/- for S&CE LWF in Kerala. Differs based on the nature of establishment

ER LWF

Rs. 20/- for S&CE LWF in Kerala. Differs based on the nature of establishment

TDS

On the Employee’s Earnings. Depends on the existing Income Tax rates

One may or may not include this as part of Employer Contributions

Table 2: Statutory Deductions on Salary

* Assumption: No other ordinarily paid allowances (other than those like OT, Performance-based incentive, etc).

Legal deductions are the savings for the retirement of your employees. Help them plan right!

So far so good. But I have read that there is a cap for EPF contributions. What is that and how is it incorporated in the salary structure?

Yes, EPF up to 12% of Rs. 15,000/-, i.e. up to Rs. 1800/- per month by Employee and Employer each is mandatory. If the (Basic + DA + Other allowances except OT, Bonus, HRA, etc.) is less than 15,000/- per month, then the EPF contribution will be less than Rs. 1800/-, which is fine. Suppose the above amount is Rs. 25,000/-. Then the 12% of 25,000 = Rs. 3000/-. The employee is not liable to pay this entire amount to EPF and can decide to cap it as Rs. 1800/-. This would mean that the employee’s EPF deduction will be Rs. 1800/- instead of Rs. 3000/-, meaning the net salary might increase since the deduction is lesser.

Another catch here is, the employer is liable to pay the equal contribution as the employee makes. So if the employee decides to cap it at Rs. 1800/-, the employer can also do the same, which may be a loss to the employee in the long term as a hole on the savings. But modern-day organisations tend to transfer the benefit of this capping to the employee, by fixing the CTC and increasing the Gross Pay to match the difference, still, all of them totalling to CTC. This would mean that the employee might get a higher net salary even if s/he caps the EPF contribution, but the transfer of benefit depends on the employer and is at their will.

Popular Posts on this Website

The post is getting longer by the minute. Would you like to conclude?

So, in short, our intention is to add up the component to Gross Pay and then add employer contributions to reach the CTC. When an offer is made (or a salary revision is recommended), companies usually look at the total cost that it would incur. The rest is on HR to design the structure in the most favorable manner.

More fun on the way

The calculation to sum up earnings, employer contributions, etc. to reach the CTC is pretty straightforward with simple arithmetic calculations. But it can become slightly complex when you are given a CTC and asked to bifurcate it to various components especially when there is a cyclic dependency is involved (e.g: ESI contribution depends on the components of the salary structure, while those components depend on the ESI contribution).

This is not rocket science and can be solved with a system of first-degree multi-variable equations. As long as we have HRMS in place, this won’t be a headache, but don’t you think it would be fun to go back to high school math and see how that helps in the above HR situations? Post your responses in the comment below and let’s see who gets it right first! Let me blog on the math later.

Salary Structuring may be an operational aspect of Human Resources, but it definitely is an important piece of the job.

I am sure your you were curious as to why the number 17,742/- for a Software Engineer when you clicked on the link to land this article. Let’s see in detail. By the way, if you are a software engineer in Kerala getting paid below this figure, it’s probably the time to send this article to your HR Manager 😉

Context

Recently, on Dec 24, 2020 to be exact, Government of Kerala announced the revised Minimum Wages for the Software industry in the state, after long 10 years of the earlier revision. Numbers have soared up. This article discusses the concept of minimum wages, with examples pertaining to Kerala state; however, the concept should be the same throughout the country.

What’s this “minimum wages”?

As the name implies, the minimum wages is the minimum wage per month to be given to an employee of a particular sector in a state. There is a national minimum wage declared by the central government, and various state-level minimum wages. The idea is to keep the state-level minimum wages equal to or above the national minimum wages. The concept of minimum wages will ensure access to equitable and justifiable pay, thereby eliminating the chances of exploitation by the management.

When is it decided?

Minimum wages are revised periodically. Minimum wages are defined for each sector separately. For example, the minimum wages for Software sector differs from that for the Oil Mills sector. There are roughly 80 such sectors identified for the State of Kerala; and similar numbers for other states as well. Governments revises the minimum wages when it deems that there is, inter alia, a significant increase in the cost of living over a period of time which is not manageable by a mere increase in Dearness Allowance (DA).

How is minimum wages calculated?

Minimum wage calculation for a role is easy. For example, look at the latest Software industry minimum wages notification for the State of Kerala below (extracted from here).

If you look at the notification, in the Software sector, roles of jobs are categorised into different grades. For instance, an HR Executive is a Group F employee in the industry, while a Software Engineer is a Group E employee. An organisation needs to categorise all their employees into one of these grades (and, if not already done by any means whatsoever before, it would be advisable to communicate the same through an HR letter/notice, through internal HR portals, payslips, etc. to the employee so that they are aware of the same) Let’s take the example of Group E: Software Engineer for illustration purpose.

Popular posts on this website

Demystifying the Minimum Wages Calculation: An Example

If you look at the Group E: Software Engineer, 16520-250-17770-300-19270 is the salary range shown for this role. What does that mean, let’s have a look!

The minimum wage for an employee who is a Software Engineer in an organisation is Rs. 16520. This amount is exclusive of another factor called Dearness Allowance (DA), which we will see about later.

Now, look at the number 250 in the wage structure. What does it signify? The notification says:

For every five years of completed or to be completed service in an establishment or under an employer, an annual increment at the rate next to the pay scale fixed in the new scale of pay shall be paid as service weightage to the employee concerned.

So, if an employee continues to be a Software Engineer under the same organisation/employer, then for every such service year, a minimum pay hike of Rs. 250/-pm should be paid as service weightage. That is, for someone with salary 16520/- as per month salary, and completed one year of service, s/he should get a minimum wage of Rs. 16520 + Rs. 250 = Rs. 16770/- pm during the second year of service. Every year, this figure per month will increase by Rs. 250/- for the first five years. Hence, s/he will have a wage of Rs. 17770/- pm during the fifth year of service. That’s the third number appearing in the pay structure.

Now, one can see a 300 next to 17770 in the pay structure. That means, we’re now done with the first five years and reached Rs. 17770/- pm as minimum wage for this employee. Hence for the next set of 5 years, the minimum wages should be increased for every service year by, not the old 250 but, Rs. 300/-. Hence, on the sixth year of service, the employee should have a minimum wage of Rs. 17770 + Rs. 300 = Rs. 18070/-. This will continue for the second block of 5 years. Hence, at the end of the 10th year (i.e. the fifth year of the second block), the employee should be getting a minimum of Rs. 19270/- pm as the salary. After the 10th year, the mandatory pay hike stops. If the employee gets promoted to a higher Grade, that’s a different story, in which case the minimum wages for that role will be applicable.

Good for them. The minimum wages talks about the minimum wages to be given, and the minimum pay hike to be given for every service years. If your pay is already above this level, then the employer is NOT obliged to give you the 250 or 300 pay hike.

Now, tell me about DA calculation?

Dearness Allowance is calculated based on an index called Consumer Price Index (CPI). I will skip the economy part and would encapsulate that it is a statistical number published by Dept of Economics and Statistics for various cities in the state, and it depicts the fluctuating cost of living. They publish it here.

DA is a mechanism provided to adjust the salaries for change in CPIs. If you look at the Minimum Wages notification, it says:

In addition to the basic rate of wages, all the employees shall be eligible for Dearness Allowance calculated on the basis of the Consumer Price Index published for the concerned District Head Quarters of the Department of Economics and Statistics at the rate of ₹ 26 (Rupees Twenty Six only) for monthly waged employees and ₹1 (Rupee One only) for daily waged employees respectively, for every point in excess of 300 points of the latest Consumer Price Index Number in the series 1998-99=100.

There are five parts to it:

DA varies for each city (read district HQ)

The rate of DA is Rs. 26/- for monthly waged employees

DA is calculated for every point in excess of 300 points

CPI is published periodically

DA for this sector is calculated basis the CPI in the Series: 1998-99=100.

With these reading in mind, let’s calculate the DA for an employee posted in Trivandrum. Look at the CPI page on the EcoStat website and choose the latest month for which CPI is available. As I write this, it is Nov 2020. If you look at the Trivandrum’s CPI value under the column Estimated Indices for Base : 2011-12 = 100 Base : 1998-99 = 100 for Nov 2020, it is 369. That’s our little guy.

Now, we need to find out the DA from this 369. As per the #3 above, DA is calculated on the CPI-300 value. Here, it is 369-300 = 69.

We need to pay Rs. 26/- per month for every point in this 69. That means, the DA per month for an employee posted in Trivandrum is Rs. 26 * 69 = Rs. 1794/-

DA is paid over and top of the above minimum wage. DA may change when CPI changes.

Tip: An organisation need NOT provide DA as a pay structure component. They can subsume DA component in the gross pay and make sure that the gross pay is above the (minimum wages + DA) figure. But it would sound problematic for organisations who use the Wage Protection System, which mandates the DA component as such, in which case one may decide to keep that little guy in the pay structure.

Are we talking about Gross Salary or Basic+DA?

With the introduction of Code on Wages, 2019 (to be in force from Apr 1, 2021), all confusions with respect to the definition of wage will vanish. You may consider the Basic + DA + Other ordinarily paid allowances (other than OT, commissions, performance-based incentive, etc.) as the wage for this purpose, meaning we’re talking about the Gross Pay. Confused about Gross Pay, CTC, etc.? I’ll write about it in my next article 😉

Compliance is a Culture.

When is this to be effective from?

This notification is to be effective from Dec 18, 2020. Even if December 2020 and/or January 2021 salaries are already paid out by the employer, they are to abide by these changes. If there are revisions to be made as per this notification, then employers have to comply and give arrears wef Dec 18, 2020.

For the existing employees, if the salaries are to be revised to comply with this notification, then the employer must take care of the service weightage as well.

Where can I see minimum wages for other sectors?

Govt of Kerala published minimum wages notifications on this page. This is the old notification for the Software Industry.

An exercise

Well, now find out the minimum wages to be paid to a Senior Software Engineer with 3.2 years of experience in the current organisation in that grade, and posted at Calicut. Post your answers in the comment box and let’s see how many of you get it right 😉

Anish asked me to write about why and how I prepared for the SHRM-CP examination so a few HRs who might not know about this certification yet could benefit. I spent some time reflecting on whether I should actually write it or not, and finally, here I’m. If it helps someone, I am happy. If not, that’s still okay 😉

Background

I am an engineer by education and early-career profession. I did my masters in Computer Science and joined Oracle in Bangalore where I spent more than 3 years doing things that I was not contented with, and that I do not consider myself good at. FullContact happened as a you-got-what-you-wished-for opportunity, and I happily accepted the offer to join there as an HR. I always loved the HR job, unlike many other engineers out there!

Well, it goes without saying that I am without an MBA. Did it matter? I will be blunt: it did matter to me, though it didn’t to my employer. I was a beginner in the HR profession, but I was invited to lead the India people division of the organisation, owing to the trust and hope the then leaders had in me. I had to make it up to it, and I did not have an MBA. Did it really matter? Does it, now?

(Image courtesy: www.peoplematters.in)

Hey dude, do you really care about the degrees (and not the skills)?

We as humans tend to see and believe things as binaries—YES or NO! Do degrees really matter? Some say that it doesn’t, and some it does. Certain degrees do really matter, but what matters more is the kind of environment you studied in and the exposure you have attained. I have seen the case studies MBA colleges use to teach the graduate students in the tier-2 colleges and the top B-schools in the country and abroad. I was well aware of the differences in engineering education, but the kind of exposure those top-tier B-schools provide to their MBA students is something unparalleled from my observation. One can’t simply say that degrees do not really matter. What matters is exposure and potential—be it with a degree or not.

One may argue that college degrees cannot provide the quantum of exposure that on-the-job training provides. While this generally true in our country, the quick(kick)start the tier-1 educated graduates get is, still, something. There’s no denying that.

Back to our story: well, I did not have a degree. My ego and self-esteem played, and I thought of doing a distance MBA, joined, fully paid for and found it to be worthless an affair, left it at that. But as time progressed, thanks to the openness and unusually solid support that I got from this organisation (and the HR communities that I am associated with such as NIPM Kerala Chapter), I could learn A LOT while being on the job. I wanted to, however, benchmark myself to see where I stood (read this as self-appraisal. Unless you benchmark yourself, you are not giving yourself feedback. If you do not give feedback often, you are buying the same fish, again).

I heard about the SHRM certification and I was not eligible to write SCP then, hence chose CP; out of the blue, after reading some online reviews. I knew that it would take some effort, but my organisation supported me by spending considerably good amount of money on this learning effort by sponsoring the digital training kit for the examination. That’s one reason why I was fast ready to write the exam.

Tell me more about the exam

There is more than enough articles on what and how the SHRM Certification examinations are, hence I will skip that part except for an excerpt:

You can write SHRM-CP if you have 2 (or, 1 for those with PG) years of professional HR experience. If you are senior in terms of service, you could try SHRM-SCP.

The test is computer-based. Continuous 4 hours (trust me, my eyes pained). 160 questions. I wrote it at Prometric centre in Trivandrum, Kerala, India.

Of the 160, there are 95 knowledge-based questions, 65 judgement questions. They are all multiple choices, but alternatives can be confusing and similar-looking. This page gives you a sample set of questions.

How I prepared: There are four books that came along with the digital learning kit that was sponsored by the organisation. I read them. They are quite helpful and one may get tons of revelations of as to how many bad concepts/understanding of HR that one has had (I did). In fact, this was the best outcome of preparing for this certification.

You will get to know your provisional results immediately after the test. They will send you the official intimation later.

The examination costs you $400 ($300 if you are an SHRM member). The certificate is valid for 3 years (and can be renewed by acquiring certain recertification points by doing online courses, attending seminars, etc.). It is not mandatory that you purchase the digital learning system. This page may be helpful.

(Image courtesy: blog.shrm.org)

Should I do it?

Yes, if you want to benchmark yourself, and maybe, study something that you already didn’t know. Or, if you are doing it as a self-confidence booster.

No, if you are just doing it for a pay hike. Mostly no organisation—I understand some may still be doing—in India provides with a pay hike for HRs just because they have a certification (but that’s not the case abroad, and some job descriptions specify these certifications as minimum requirements, which is a benchmarking/filtering tactic). However, it can be a distinguishing factor. After all these, I know in person a ton of HR professionals doing much better than me, without an MBA and/or an SHRM Certification. So, it’s just all about what you want.

If you’re not so concerned about the certification, why have you written “SHRM-CP” in your LinkedIn profile name?

I am just being ostentatious.

So, you’re saying that you’re after fancy degrees (or candidates with such degrees)?

Wait there, never did I say that I have high respect for candidates just with fancy degrees. Moreover, I believe in interviews that are based on Behavioral Competencies (from a People standpoint)—BEI as it is called—rather than education texts that fill in white spaces on a resume.

TL;DR: Take an SHRM certification exam (or its competitor HRCI) if you want to benchmark yourself against what is considerably-okay in the industry. You may gain some confidence, too.

Wait, did I write a TL;DR at the bottom? 😉

P.S: Julian has written about how he passed the examination already, my job is reduced by 90% in writing this article and hence not explaining what he has already done.

P.P.S: I would strongly recommend being part of the SHRM community by spending money on their membership. It is really worth it (an online membership would suffice) in terms of strategic/operational documentation that is available on their member-only portal and the community of HRs they have built.

If you have more questions, I am happy to help. Please drop me a message or write in comments (beware: you are going to talk to someone who is known to be incommunicado for longer durations; so please expect the delay).